Cameco Corporation (CCJ), Denison Mines Corp. (DNN), enCore Energy Corp. (EU) IsoEnergy Ltd. (ISOU), Centrus Energy Corp. (LEU), NexGen Energy Ltd. (NXE), Uranium Energy Corp. (UEC), Ur-Energy Inc. (URG), Uranium Royalty Corp. (UROY), Energy Fuels Inc. (UUUU)

The upstream uranium industry encompasses uranium exploration, mining, and enrichment, which together produce the nuclear fuel for power reactors. Uranium mining yields uranium oxide concentrate (U₃O₈) – commonly called yellowcake – which is then converted to uranium hexafluoride and enriched to increase the fissile U-235 content for reactor fuel. This segment is critical in the nuclear energy supply chain, providing the raw material that fuels roughly 440 reactors worldwide and underpins ~10% of global electricity generation. Nearly all uranium is used for electricity (with a minor fraction for medical isotopes and naval propulsion). After a decade-long post-Fukushima slump, the industry is now rebounding to meet rising nuclear demand driven by climate goals and energy security needs.

Current supply and demand: Global uranium demand in 2024 was about 67,000 tonnes U per year (≈148 million lbs U₃O₈), exceeding primary mine production (which was ~60,000 t in 2024). The shortfall is bridged by secondary sources (inventories, downblended warheads, reprocessed fuel). For example, production in 2023 was ~165 million lbs versus ~180 million lbs consumed, a 15 million lb deficit made up from stockpiles. This structural deficit emerged after years of low prices that curtailed mine output.

Major producers and concentration: Uranium mining is highly concentrated geographically and corporately. Just 10 mines in 4 countries account for over 60% of world output. Kazakhstan and Canada alone supply the majority: Kazakhstan contributes ~40% of world uranium (mostly via low-cost in-situ leach mines), while Canada’s high-grade Athabasca Basin mines provide ~24%. Namibia, Australia, and Uzbekistan are other key producers. This concentration creates geopolitical risk in supply. For instance, Kazakhstan’s dominance (with about 40% share) and Russia’s role in uranium processing have prompted consumer nations to seek diversified sources. The upstream segment thus sits at a strategic nexus of energy and geopolitics, ensuring fuel supply for nuclear reactors worldwide.

Role of enrichment: After mining, natural uranium (only ~0.7% U-235) must be enriched to ~3–5% U-235 for use in typical reactors. Enrichment (via centrifuges) is often considered a separate mid-stream step, but is part of the upstream fuel cycle for our purposes. Only a few companies (e.g. Urenco, Orano, Tenex, and in the U.S., Centrus) provide enrichment services. Enrichment capacity has historically been ample, but with new reactor designs needing high-assay LEU and potential restrictions on Russian enrichment, this segment is gaining strategic importance. Overall, the uranium upstream industry’s output – uranium concentrate and enriched uranium – is the indispensable first link in the nuclear fuel supply chain, enabling the operation of nuclear power plants around the globe.

🏭 Key Companies

Cameco Corporation (CCJ) – Tier-1 Producer and Integrator

Market Position: Cameco is one of the world’s largest uranium producers and the dominant western-based uranium company. It operates tier-1 mines in Canada’s Athabasca Basin, including McArthur River and Cigar Lake – two of the top-producing uranium mines globally. In 2024, McArthur River/Key Lake produced ~7,808 tU (13% of world mine output) and Cigar Lake ~6,501 tU (11% of world output), illustrating Cameco’s significance. The company also owns 40% of the Inkai ISR mine in Kazakhstan. Cameco has a vertically integrated footprint with uranium refining/conversion capacity and recently expanded into nuclear services. It benefits from large high-grade reserves, low unit costs, and a strong contract book with utilities worldwide.

Recent Strategic Moves: Cameco has pursued a strategy of supply discipline and downstream integration. Notably, it idled capacity during the low-price years and only restarted the McArthur River mine in late 2022 as market conditions improved. This helped tighten supply and positioned Cameco to capture upside as prices rose. On the integration front, in Nov 2023 Cameco (49%) and Brookfield Renewable (51%) acquired Westinghouse Electric, a major nuclear fuel and reactor services company. This transformative deal gives Cameco exposure to reactor fuel fabrication and services, creating a broader “fuel cycle” platform for growth. Cameco has also been aggressively contracting uranium with utilities at higher prices to lock in long-term sales. As of year-end 2024, it had ~220 million lbs in its long-term delivery backlog through 2029 – providing revenue visibility and insulation from spot price volatility. The company’s average realized uranium price in 2024 was $79.70/lb on 33.6 million lbs sold, reflecting strong markets and its contracting success.

Centrus Energy Corp. (LEU) – Advanced Enrichment Specialist

Market Position: Centrus (formerly USEC Inc.) is a U.S.-based nuclear fuel company focused on uranium enrichment and advanced fuels. It is currently the only American company with licensed enrichment capability. Centrus does not mine uranium; instead, it provides enrichment services and is poised to supply High-Assay Low-Enriched Uranium (HALEU) needed for many next-generation reactors. This niche – enrichment to >5% U-235 – positions Centrus as a critical player in future fuel supply for small modular reactors and advanced designs. The company has a long history in enrichment technology (centrifuges) and maintains the only U.S. enrichment plant (the AC100 centrifuge cascade in Ohio) on standby. Centrus also brokers LEU and provides nuclear fuel consulting.

Recent Strategic Moves: Centrus’ key move has been executing a U.S. Department of Energy contract to domestically produce HALEU. In late 2023, Centrus successfully produced an initial 20 kg of HALEU under a DOE demonstration contract – the first U.S. HALEU production in decades. The DOE recently extended Centrus’ contract through 2026 to continue HALEU production and scale up output. This firmly establishes Centrus as a government-backed supplier for advanced reactor fuel. Financially, Centrus has swung to profitability on the back of this contract: it achieved a 22.7% EBITDA margin over the last 12 months and a ROTC of ~10.7% – among the highest in the peer group – thanks to high-value enrichment revenues. The company is also exploring commercial HALEU supply agreements with advanced reactor developers. Centrus’ strategy is to leverage its enrichment technology leadership and government support to capture the emerging HALEU market, while continuing its legacy LEU supply business. This capital-light, service-oriented model has made Centrus one of the most capital-efficient, cash-generative companies in the sector despite its small size.

Denison Mines Corp. (DNN) – Developer of High-Grade Canadian Uranium

Market Position: Denison Mines is a uranium development and exploration company headquartered in Canada. It holds a large portfolio of projects in the Athabasca Basin, including a 95% stake in the Wheeler River Project – host to the high-grade Phoenix and Gryphon uranium deposits. Phoenix, in particular, has extremely high grades (averaging ~19% U₃O₈) and is envisioned as the first in-situ recovery (ISR) mining operation in the Athabasca region. Denison also has a 22.5% ownership in the McClean Lake mill (which currently processes ore from Cigar Lake) and manages uranium exploration across several other properties. While Denison currently has minimal production (and thus negligible revenue), its asset base boasts over 300 million lbs U₃O₈ in resources and significant potential future output if developed.

Recent Strategic Moves: Denison’s strategy is focused on advancing Wheeler River (Phoenix deposit) toward production using innovative mining methods. In 2022, Denison completed a highly successful ISR field test at Phoenix, confirming that uranium-bearing solution could be recovered from the orebody. This de-risked the planned ISR approach in the high-grade deposit. Subsequently, in mid-2023 Denison published a Feasibility Study for Phoenix ISR mining, reporting robust project economics. The company has also consolidated ownership of Wheeler River – increasing its stake to 95% – by acquiring minority partner interests, which gives it greater control over development. On the financing side, Denison in 2021 sold a 2.5% net smelter royalty on Wheeler River to Anglo Pacific for $40.5 million, raising cash for project advancement. More recently, Denison fortified its balance sheet by equity financings to fund environmental permitting and engineering. With the uranium market improving, Denison is positioning to make a construction decision in the next couple of years. It aims to bring Phoenix into production by the late 2020s, targeting initial output of ~6 million lbs U₃O₈ per year.

enCore Energy Corp. (EU) – Emerging U.S. In-Situ Producer via Acquisitions

Market Position: enCore Energy is a U.S.-focused uranium company rapidly growing into a near-term producer through in-situ recovery (ISR) projects. In just a few years, enCore has gone from a junior explorer to controlling multiple fully licensed ISR production facilities in the United States. Its key assets include the Rosita processing plant in South Texas (started production in 2023) and the Alta Mesa ISR central plant in Texas, which it acquired and re-started in 2024. EnCore also holds the advanced Dewey-Burdock ISR project in South Dakota and the Gas Hills project in Wyoming (acquired via its 2022 merger with Azarga Uranium). This portfolio gives enCore one of the largest ISR project pipelines in North America. The company’s strategy is to become a leading domestic uranium producer by sequentially bringing these facilities online.

Recent Strategic Moves: enCore’s growth has been driven by M&A and project restarts. In early 2023, it acquired the Alta Mesa ISR plant and resources from Energy Fuels for $120 million, adding a fully built production center. Alta Mesa had produced ~5 million lbs U₃O₈ between 2005–2013 before being idled due to low prices. EnCore swiftly refurbished Alta Mesa and resumed production there in 2024. In fact, Q4 2024 output at Alta Mesa was 127,293 lbs U₃O₈, making enCore the second-largest uranium producer in the U.S. for that quarter. The company installed a second ion-exchange circuit at Alta Mesa to double its flow capacity and is expanding wellfields to boost output in 2025. Meanwhile, enCore’s Rosita plant in Texas began producing uranium in 2023 and continues to operate. To fund these endeavors, enCore secured a strategic $70 million financing from Boss Energy (an Australian producer) in 2023. The company is also progressing permitting at Dewey-Burdock (final EPA permits received) and plans to develop Gas Hills. In summary, enCore has grown via acquisition of ready-to-produce assets and aggressive project re-starts. This has transitioned the company into an active producer: in 2024 it produced ~0.13M lbs in Q4 alone and expects significantly more in 2025 with Alta Mesa’s expansion. EnCore’s strategic focus is on quickly ramping ISR production across multiple sites to establish itself as a top US uranium supplier.

NexGen Energy Ltd. - Peer with the largest upside

Market position: Its flagship Rook I project in Saskatchewan’s Athabasca Basin – centered on the high-grade Arrow deposit – ranks among the largest undeveloped uranium resources globally. NexGen’s business model is to advance such discoveries through permitting and mine development; Rook I is currently the largest development-stage uranium project in Canada, underscoring the company’s role at the exploration and development end of the uranium value chain.

Due to the Arrow deposit’s scale and exceptionally high grades, NexGen is poised to become a major supplier in the global uranium sector. Rook I is expected to produce roughly 25–30 million pounds - approximately a quarter of current worldwide uranium mine output - while operating at lowest-quartile production costs. This combination of volume and cost position would make NexGen one of the largest and lowest-cost uranium producers once the mine is operational.

Recent Strategic Moves: In recent years, NexGen has made significant strides toward bringing Rook I into production. The company secured provincial environmental approval in 2023 and, as of late 2024, successfully completed the federal technical review process, with final licensing hearings scheduled for 2025–2026. NexGen also finished front-end engineering design (FEED) in mid-2024 and initiated detailed engineering and site preparations, aiming to begin full construction promptly upon receiving final federal approval. In addition, the company signed its first long-term uranium sales contracts in late 2024, agreeing to supply 5 million pounds to major U.S. utilities (approximately 1 million lbs annually from 2029 to 2033). These initial offtake agreements demonstrate market confidence in NexGen’s project and help backstop the financing needed for mine development.

IsoEnergy Ltd. (ISOU) – High-Grade Explorer Turning Producer via Merger

Market Position: IsoEnergy began as a uranium exploration company focused on high-grade discoveries in the Athabasca Basin (Canada). It is known for the 2018 discovery of the Hurricane deposit – a near-surface, very high-grade uranium zone (up to 70% U₃O₈ in drill assays) on its Larocque East property. While exploration remains a core strength, IsoEnergy is now transforming into a development-stage and production-capable company. In late 2024, IsoEnergy announced the acquisition of Anfield Energy, which brings a portfolio of U.S. conventional uranium assets and importantly the Shootaring Canyon Mill in Utah. Shootaring is one of only three licensed uranium mills in the U.S. This merger (expected to close in 2025) significantly expands IsoEnergy’s asset base beyond Canada, giving it near-term production potential in the Western U.S.

Recent Strategic Moves: The planned acquisition of Anfield Energy (AEC) is IsoEnergy’s most notable move. Announced in October 2024, this deal will secure IsoEnergy 100% ownership of the Shootaring Canyon Mill plus Anfield’s conventional uranium/vanadium projects in Utah, Colorado, and Arizona. The strategic rationale is to create a “multi-asset uranium producer” with a combined U.S. project portfolio that can feed Shootaring (which is being permitted for a throughput increase to 1,000 tpd and 3M lbs U₃O₈ annual capacity). The merger expands IsoEnergy’s resource base by +157% (to 17.0 Mlbs M&I in the U.S.) and positions the company among the largest uranium holders in the U.S. Even ahead of the merger, IsoEnergy signaled its production ambitions by restarting work at the past-producing Tony M Mine in Utah (one of Anfield’s assets). In May 2025, IsoEnergy (traded as ISOU on NYSE) launched programs to evaluate and advance the Tony M uranium mine, which had operated in the 1970s–80s. This is a pivot from pure exploration to re-developing brownfield mines. Concurrently, IsoEnergy continues advancing its high-grade Hurricane deposit toward economic studies, and it raised ~$15M in 2023 to support exploration and development. In summary, IsoEnergy’s recent strategy is a bold pivot from explorer to producer: by acquiring Anfield, it gains near-term production capability in the U.S. (with a mill and permitted mines) while retaining upside from its Canadian high-grade projects. This diversification aims to make IsoEnergy a future mid-tier uranium producer spanning multiple jurisdictions.

Uranium Energy Corp. (UEC) – Aggressive Consolidator with ISR & Conventional Projects

Market Position: Uranium Energy Corp is a U.S.-based uranium company that has pursued an aggressive growth-by-acquisition strategy, assembling a broad portfolio of production-ready and development assets across the United States, Canada, and Paraguay. UEC’s core holdings include ISR operations in South Texas (the Palangana mine and Hobson processing plant, Burke Hollow development) and in Wyoming (the Reno Creek project, and recently restarted operations at Christensen Ranch/Irigaray). UEC has also acquired significant conventional project assets – notably, it acquired Uranium One Americas’ U.S. in-situ assets in 2021 and bought Canada’s UEX Corporation in 2022, which brought a suite of Athabasca Basin projects. Through UEX, UEC obtained 100% of the advanced Roughrider deposit (an Eastern Athabasca development project acquired from Rio Tinto) and minority stakes in other Canadian deposits. As a result, UEC now touts one of the largest resource bases among junior uranium companies, with diversified projects ranging from near-term ISR production in the U.S. to longer-term high-grade projects in Canada. The company has also stockpiled physical uranium (over 1 million lbs) as a strategic reserve.

Recent Strategic Moves: UEC’s strategy has been characterized by serial acquisitions and project restarts:

In 2021, UEC purchased Uranium One’s entire U.S. asset portfolio (including the Christensen Ranch/Irigaray ISR processing plant and licensed Wyoming resources). This instantly expanded UEC’s production capability in Wyoming.

In mid-2022, UEC outbid competitors to acquire UEX Corporation, doubling UEC’s resources and giving it stakes in multiple Canadian deposits. Notably, Roughrider is a world-class deposit (17.2 Mlbs @ 4.0% U₃O₈ indicated) that UEC is now advancing; a preliminary economic assessment in 2023 showed it could be a top-tier underground mine.

UEC completed the Roughrider acquisition from Rio Tinto in Oct 2022 for $150 million, consolidating 100% ownership.

Operationally, UEC resumed ISR production in 2023–24. In South Texas, it maintained Palangana on standby (and built a uranium inventory by buying in the spot market). In Wyoming, UEC restarted the Christensen Ranch ISR wellfield in August 2024 (first production there since 2018), and by early 2025 it had drummed its first pounds from this restart. UEC is now ramping up wellfield flow rates and could become a producer in 2025. It also received its final permits for the Burke Hollow ISR project in Texas, positioning that for future output.

To fund these moves, UEC has leveraged its strong market capitalization to raise capital (it raised over $250M in 2021–22). Notably, UEC strategically held a physical uranium inventory (2.3 Mlbs at one point) which it has used to monetize gains or collateralize deals – a different tactic than most peers.

Ur‐Energy Inc. (URG) – Established Small Producer with ISR Operations in Wyoming

Market Position: Ur‑Energy is a U.S. uranium mining company operating in Wyoming. It is among the few American firms that achieved commercial production in the 2010s. Ur‑Energy’s flagship asset is the Lost Creek ISR mine and plant, which began production in 2013. Lost Creek has licensed capacity of ~2 million lbs U₃O₈ per year, though it operated at reduced rates and was idled during the low-price period. Ur‑Energy also fully permits the Shirley Basin ISR project (Wyoming), a near-term development expected online by 2026. Shirley Basin was a past-producing district now being advanced with modern ISR methods. Ur‑Energy’s resources are more modest than some peers (~11.9 Mlbs proven & probable at Lost Creek, 8.8 Mlbs P&P at Shirley Basin), but it has the advantage of fully constructed and permitted processing infrastructure at Lost Creek. Overall, Ur‑Energy is positioned as a low-volume but flexible producer, focused on U.S. domestic supply.

Recent Strategic Moves: After weathering several years of minimal activity, Ur‑Energy is now ramping up production in response to higher prices and new contracts:

In 2021–2022, Ur‑Energy kept Lost Creek on care-and-maintenance (and reported zero uranium sales in those years) to conserve resources while prices were low. It used this time to optimize wellfields and cut costs.

In late 2022, with uranium markets improving, Ur‑Energy secured multiple long-term contracts with U.S. utilities. As of 2023, it had seven contracts for deliveries totaling 440,000–1,300,000 lbs U₃O₈ annually from 2025–2030. This base of committed sales gave Ur‑Energy confidence to restart mining.

The company resumed production at Lost Creek in Q2 2023. By 2024, it produced 570,000 lbs (0.57 Mlbs) and generated $33.7M revenue from sales – a dramatic rebound from nil production previously. In fact, Ur‑Energy was the largest uranium producer in the U.S. for full-year 2024 (despite being surpassed by others in Q4 output).

Ur‑Energy also participated in the U.S. government’s Uranium Reserve program: in 2023 it sold 280,000 lbs to the DOE for ~$18M. These government purchases (at ~$64/lb) provided a timely cash infusion.

On the expansion front, Ur‑Energy commenced construction at Shirley Basin in 2023. Shirley Basin is expected to begin production by January 2026 and will add ~0.8–1.0 Mlbs/year of capacity (an ~83% increase in company-wide licensed output). This project has a shorter mine life but very low-cost, shallow ore.

To strengthen its balance sheet, Ur‑Energy raised ~$45M equity in 2023 and paid down debt. It entered 2025 with ample cash to fund the Shirley Basin build-out.

Uranium Royalty Corp. (UROY) – Royalty & Streaming Play on Uranium Assets

Market Position: Uranium Royalty Corp (URC) is the only pure-play uranium royalty and streaming company. Rather than mining directly, URC provides financing to uranium mine developers/operators in exchange for royalties (a percentage of production or revenue) or streams (rights to purchase a portion of production at a fixed price). URC has assembled a portfolio of interests in several prominent uranium projects: e.g. a 1.97% NSR royalty on the McArthur River mine (Canada), 3.0% NSR on Cigar Lake (Canada) via a holding, 7.5% gross revenue royalty on Langer Heinrich (Namibia), and various royalties on development projects in the U.S. (Dewey-Burdock, Lance) and elsewhere. The company also holds physical uranium inventory (over 1.5 million lbs U₃O₈) and equity stakes in uranium companies. Uranium Royalty’s model offers investors exposure to uranium price upside and project success without direct operating risks or costs – making it akin to royalty companies in gold or oil.

Recent Strategic Moves: Uranium Royalty Corp has been actively deploying capital into royalties, strategic equity, and physical uranium:

It has acquired royalties on several producing mines. In 2022, URC purchased a portfolio of royalties from Rio Tinto, including the McArthur River royalty, for ~$26M. As McArthur resumed production in 2022–2024, URC began receiving royalty revenue from this top-tier mine. Similarly, with Paladin’s Langer Heinrich mine restarting in 2024, URC’s royalty on that asset will start generating cash flow.

URC built up a significant physical uranium inventory at attractive prices. It bought ~1.4 million lbs U₃O₈ in 2021–2022 at an average ~$42/lb. In fiscal 2023, as prices rose, URC opportunistically sold a portion (300,000 lbs) of its inventory at ~$50–$60/lb, realizing a profit and bolstering its cash. This contributed to URC’s revenue in that period. However, such sales are one-off in nature.

The company raised $25M in mid-2023 via equity to fund further royalty acquisitions and maintain a strong treasury for new deals. It also increased its stake in Yellow Cake plc (a London-listed physical uranium holding company), enhancing its indirect uranium exposure.

Uranium Royalty’s strategy is to continue adding royalties on high-quality projects. It announced in 2023 a new royalty on the Dawn Lake project (Saskatchewan) and is eyeing other investments, benefiting from its insider relationships (it has close ties to NexGen and other developers via shared major shareholders).

Financially, URC’s revenues have been relatively small (FY2024 revenue ~$7M, largely from uranium sales and interest). The volatility of its income is notable – for instance, after a one-time uranium sale boosted 2024 revenue, analysts forecast a ~71% drop in revenue for 2025 since fewer transactions/royalty payments are scheduled. Despite negative net earnings (common for a growth-stage royalty firm), URC’s free cash flow margin has been positive (about +44% LTM) because its operating expenses are low and it can generate cash by liquidating uranium inventory.

Energy Fuels Inc. (UUUU) – U.S. Uranium Producer Diversifying into Rare Earths

Market Position: Energy Fuels is a unique player in that it is the leading U.S. producer of conventional (hard-rock) uranium and has recently diversified into rare earth element (REE) processing. The company owns the White Mesa Mill in Utah, which is the only operating conventional uranium mill in the United States. This mill gives Energy Fuels the ability to process uranium ore from its own mines and alternate feeds (materials like cleanup wastes and mineral sands). Energy Fuels holds a portfolio of uranium mines primarily in the Four Corners region (Utah/Arizona/Colorado), including Pinyon Plain (Arizona), La Sal Complex (Utah), and Whirlwind & others (Colorado), mostly on standby during low uranium prices. It also has significant vanadium resources (a vanadium processing circuit at White Mesa) and began processing monazite sands at White Mesa in 2021 to produce a mixed REE carbonate – positioning itself in the critical minerals supply chain. Energy Fuels thus has a multi-commodity portfolio, but uranium remains a core focus, especially as it typically contributes the bulk of revenue when in production.

Recent Strategic Moves: Energy Fuels’ strategy in recent years has been two-pronged: restart uranium production as markets improve, and invest in rare earth processing capability for additional revenue streams:

Restarting Uranium Mining: In 2022–2023, with rising prices, Energy Fuels reopened some of its mines. It resumed mining at the Pinyon Plain mine (formerly Canyon mine) in Arizona in 2022, stockpiling high-grade ore. It also restarted operations at its La Sal and Pandora mines in Utah to generate feed for White Mesa. By late 2024, Energy Fuels was actively processing these ores: in Q4 2024, it produced 157,525 lbs U₃O₈ at White Mesa, making it the top U.S. producer for that quarter. For full-year 2024, Energy Fuels was the third-largest U.S. uranium producer (after Ur‑Energy and enCore) with ~0.16 Mlbs, all produced in Q4. The company is also preparing its Nichols Ranch ISR project (Wyoming) for potential restart within ~12 months if market conditions warrant, signaling readiness to further boost production.

Rare Earth Initiatives: In a notable pivot, Energy Fuels entered the rare earth elements arena. It struck a deal with Chemours to acquire and process monazite sands (which contain uranium and rare earths). Since 2021, White Mesa Mill has been processing monazite ore from Georgia to extract uranium (a by-product) and produce a mixed rare earth carbonate. In 2022, Energy Fuels acquired the Alta Mesa heavy mineral sand project in Brazil (from vendor Ionic Sands, often referred to as acquiring assets from Base Resources) to secure monazite supply. In 2024, REE processing contributed significantly: the company sold ~$16.9M of REE carbonate in Q1 2025. It is working to install separation circuits to move further down the REE value chain (aiming to produce separated oxides in the future). This diversification is part of a U.S. government-backed effort to establish domestic REE capabilities and has garnered Energy Fuels some DOE funding and contracts.

Financial moves: Energy Fuels took advantage of high vanadium prices in 2018–2019 to sell vanadium inventory and bolster cash. More recently, it raised ~$88M in equity in 2021 to fund rare earth and uranium project developments. It also sold its non-core Alta Mesa ISR project to enCore for $120M in 2023, monetizing an asset that was idle and using proceeds to focus on its core (this sale ironically helped enCore become a producer).

The net result of these moves is that Energy Fuels has evolved into a multifaceted company. It can generate revenue from uranium, vanadium, and rare earths, which gives it flexibility but also introduces earnings volatility.

🤼 Competitor Strategy Comparison – Current Tactics and Differences

The above companies employ a range of strategies in the upstream uranium sector, shaped by their asset profiles and corporate objectives. A comparison of their current strategies highlights several distinct approaches:

Large Producer vs. Junior Developer: Cameco represents the large, established producer strategy – it practices production discipline and long-term contracting. Cameco carefully matches output to contracts and even held back production during the glut years, preserving asset value. Its focus now is on securing long-term supply agreements (220 Mlbs contracted through 2029) and expanding vertically (e.g. via Westinghouse acquisition) to offer full fuel services. In contrast, most juniors (e.g. NexGen, Denison, IsoEnergy) are still in project development mode – they prioritize permitting, feasibility studies, and strategic partnerships/financing to eventually bring their first mines online. These developers typically do not hedge or contract much yet, preferring to keep future production uncommitted to ride expected price increases. Their tactical focus is on de-risking projects (e.g. Denison’s ISR field tests) and securing funding (NexGen’s large strategic investment from Asia, etc.) to achieve construction.

Growth by Acquisition vs. Organic Growth: Several mid-tier companies are pursuing growth-through-acquisition strategies. Uranium Energy Corp (UEC) and enCore Energy exemplify this by rapidly buying up assets to scale their resource base and production capacity. UEC acquired entire portfolios (Uranium One, UEX) to become a one-stop shop with multiple projects, and enCore bought Alta Mesa and Azarga’s assets to quickly become a producer. This contrasts with an organic growth strategy seen at companies like Ur-Energy or historically Cameco – Ur-Energy largely stuck to developing its own Lost Creek and Shirley Basin, expanding stepwise as market signals turned positive. The acquisitive companies aim for fast-track growth, banking on readily deployable assets to leapfrog into production, whereas organic growers tend to be more cautious, scaling output gradually in line with contract cover or price floors.

U.S. Domestic Focus vs. International Diversification: Energy Fuels, Ur-Energy, enCore, UEC all emphasize a U.S. production revival, leveraging increasing U.S. government support (uranium reserve purchases, potential import tariffs, etc.) to justify restarts. Their tactics include engaging in U.S. federal initiatives (e.g. Ur-Energy and Energy Fuels sold into the U.S. Uranium Reserve at premium prices) and highlighting “America-first” supply security in investor messaging. In contrast, Cameco and NexGen (Canada-focused) or those with international portfolios (UEC with Canadian projects, Uranium Royalty with global royalties) are more globally diversified in outlook. They target utility customers worldwide and may not rely on any single country’s policy. For example, Cameco’s contracts span Asia, Europe, Americas, and it formed a JV with a UK firm (Brookfield) for Westinghouse to globalize its services. Meanwhile, U.S.-centric players like enCore and Ur-Energy timed their production restarts partly on favorable U.S. policy signals (fast-tracked permitting, etc.) and are tailoring growth to meet potential U.S. utility demand surges (e.g. data center energy needs driving U.S. uranium consumption).

Contracting and Market Exposure: Strategy also diverges on market approach. Cameco and Ur-Energy favor long-term contracts to ensure stable cash flow and fund operations – Cameco’s backlog insulates it from short-term price swings, and Ur-Energy signed multi-year deals before ramping Lost Creek. In contrast, some peers have been more spot-exposed or speculative. For instance, Energy Fuels and Ur-Energy withheld sales in years of low prices and sat on inventory, waiting for higher spot prices. This opportunistic approach can yield higher prices for their product when the market improves, but also means absorbing holding costs and operational shutdowns during downturns. Similarly, developers like NexGen/Denison have no contracts yet – implicitly a bet on future higher spot/term prices (they intend to secure contracts closer to production). Uranium Royalty Corp’s strategy is purely a leveraged price exposure play – it buys physical uranium and royalties instead of engaging in contracts, to maximize upside when uranium prices rise. Each approach balances risk differently: contract-heavy strategies trade some upside for certainty (suitable for large producers needing stable revenue), while spot-exposed strategies aim to capture maximum upside at the cost of near-term volatility.

Technology and Niche Focus: A unique strategic differentiator is technological niche:

Centrus stands out by focusing on enrichment technology (HALEU) rather than competing in mining. Its tactic is to align with government programs (DOE HALEU contract) and position itself as an indispensable supplier in the advanced reactor supply chain. This contrasts with all the miners who are competing in the arena of finding and extracting U₃O₈. Centrus essentially sidesteps the mining rush and instead bets on a niche where it has limited competition (Western enrichment capacity) – a very different competitive arena than the mining-focused companies.

Energy Fuels carved a niche in critical minerals diversification – it uses its existing infrastructure for rare earth processing, giving it a second revenue stream distinct from pure uranium mining. This tactical pivot aims to utilize its mill year-round (processing monazite for REEs even when uranium ore supply is low) and to leverage U.S. government support for rare earth independence. No other peer in this list has entered the rare earth market; it’s a differentiator for Energy Fuels but also means managing two commodity markets (with different dynamics) under one roof, which can be challenging.

📈 Historical and Forecast Growth Performance

The past five years have seen starkly different revenue trajectories among these companies, largely reflecting their operational status (producer vs. developer) and market conditions. Broadly, companies that resumed or began production during the uranium price upswing have demonstrated explosive revenue growth, while those still in pre-production or idled saw flat or declining revenues:

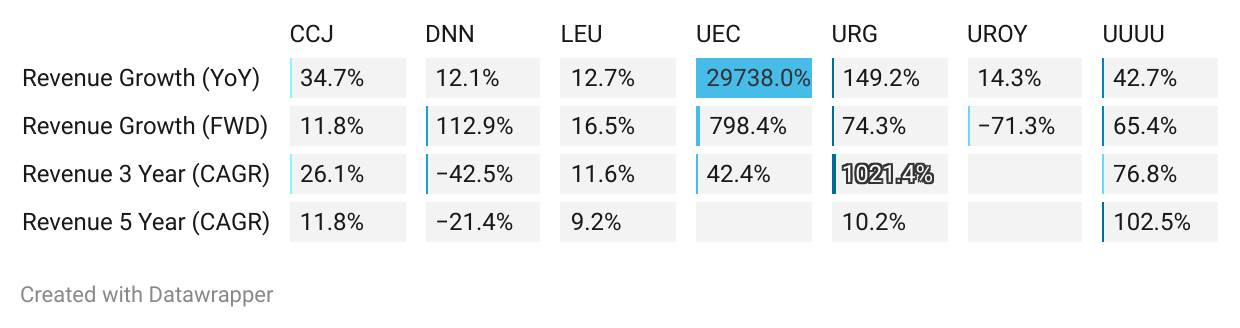

Leaders in past 5-year growth: Energy Fuels and Uranium Energy Corp stand out for extraordinary percentage growth (albeit from tiny bases). Energy Fuels’ revenue rocketed from just $3 million in 2021 (when it made no uranium sales) to over $78 million in 2024. This equates to a 5-year CAGR over 100% and ~26x increase, driven by the company’s re-entry into production and new rare earth sales. Uranium Energy Corp similarly went from essentially zero mining revenue (it had been idle, focusing on acquisitions) to tens of millions in sales after 2022–2023 as it sold inventory and restarted wellfields – a year-on-year growth of 29,738% was recorded in the last year alone. Ur‑Energy also showed high growth: after no sales for years, it recorded $33.7M revenue in 2024 by selling 570,000 lbs, up from $0 in 2021–2022, which yields an astronomical CAGR (Ur‑Energy’s 3-year revenue CAGR is over 1000%). Essentially, any company that went from 0 to active production exhibits huge percentage gains.

Middle-of-pack growth: Cameco achieved solid growth on an already large base. From 2019 to 2024, Cameco’s revenue grew at roughly 11.8% CAGR. Notably, from 2021 to 2024, it accelerated to ~24.8% CAGR as it brought McArthur River back online and uranium prices rose. In fact, Cameco’s 2025 revenue is forecast around C$3.3–3.55 billion, which would be ~30% CAGR over 2021–2025 – a robust growth trajectory for a major producer. Centrus Energy’s revenue grew around 9–12% annually in recent years, reflecting its steady but niche enrichment services (with a bump in 2023 due to the HALEU contract). Uranium Royalty Corp saw modest revenue growth (from small royalty and trading income) – one dataset showed +14% y/y – but its revenue levels remain low and irregular.

Laggards in past growth: Development-stage companies without production unsurprisingly had negligible or negative revenue growth. Denison Mines, for example, saw a decline in its small revenues (derived from toll milling and management fees) – its 5-year revenue CAGR was about -21%. IsoEnergy and NexGen have essentially no revenue in this period (only interest income or minor option payments), so they don’t register meaningful growth. These firms were effectively in R&D mode, not generating operating income yet, hence “growth” in the conventional sense doesn’t apply until they begin production. Anfield Energy likewise had no revenue and remained at zero.

Expected revenue growth (2025–2030): Over the next five years, the consensus expectation is that as new projects come online, many of these companies will transition from zero revenue to substantial sales, making them the growth leaders, while established players grow more moderately. Key projections and assumptions include:

High future growth potential (developers turning producers): Companies like NexGen and Denison are poised for transformational revenue growth once their flagship mines commence production (targeting around 2027–2028 for NexGen’s Arrow and ~2026–2027 for Denison’s Phoenix). For example, NexGen’s Rook I (Arrow) is forecast to produce ~25–30 Mlbs annually at peak – nearly a quarter of current world demand – which would propel NexGen’s revenue from $0 to perhaps ~$1.5–2 billion/year (if uranium prices ~$60–$70/lb). That is effectively infinite percentage growth from today. Denison, with a smaller Phoenix ISR operation (~6 Mlbs/year planned), could likewise see revenue jump from near $0 to hundreds of millions annually post-2026. The market views these as high-upside, high-growth companies, but that growth is back-end loaded (late this decade). Even in the near-term, early revenue trickles may start: Denison, for instance, is expected to more than double its revenue in 2025 (+113% y/y) as it potentially sells some of its produced resin from ISR field tests or receives one-time payments. But those initial revenues are tiny – the real surge awaits full production.

Steady growth for current producers: Cameco is expected to continue growing but at a more moderate pace now that its main capacity is online. Analysts project Cameco’s revenue will rise ~11% in 2025 and the company itself forecasts ~4–5% annual volume growth through 2028 (with McArthur River at full rate and potential incremental increases). If uranium prices continue climbing, Cameco’s top-line could grow faster (since many of its contracts are market-linked). But relative to the triple-digit bursts of smaller players, Cameco will likely see low-double-digit annual growth – still industry-leading in absolute dollar terms, but not in percentage. Centrus Energy should see healthy growth (~16% in forward 1-year revenue as it expands HALEU production under the extended DOE contract. Its five-year growth will depend on commercial HALEU demand; if advanced reactors proceed, Centrus could scale its cascade (with DOE cost-sharing) and significantly increase revenue by 2026–2030. For now, a mid-teens annual growth rate is anticipated for Centrus – solid but not explosive.

Ramping juniors to lead near-term % growth: In the immediate next 1–2 years, U.S. ISR producers like UEC, enCore, Ur-Energy are set to deliver some of the highest percentage revenue growth as they ramp up output from a small base:

Uranium Energy Corp’s revenue is projected to jump ~813% in the next year, reflecting that it will likely move from sporadic sales to steady contract deliveries (especially if it begins selling from its Wyoming operations and newly acquired inventories). Over a five-year span, UEC could become a mid-tier producer with multiple millions of pounds sold annually, implying continued high CAGR (though the initial spike is largest).

enCore Energy, having just begun production in 2023–24, should also see multi-fold revenue increases. Its Alta Mesa plant is scaling up (doubling flow capacity), and the company could add Dewey-Burdock output before 2030. We could see enCore’s annual revenue grow from a few million in 2024 to perhaps >$50M by 2026 and higher beyond – a very high CAGR. (Specific consensus figures are not widely available due to its early stage, but clearly the growth trajectory is steep.)

Ur‑Energy, thanks to its new contracts, will likely roughly double its revenue in 2025 (+74% y/y forecast) and continue growing as it adds Shirley Basin’s output by 2026. Having sold ~$33M in 2024, Ur‑Energy’s annual sales could increase to ~$50–60M in a couple years, then possibly ~$80M+ once Shirley Basin is at capacity, representing strong growth (though not as extreme as those starting from zero).

Energy Fuels might see sizable growth as well, albeit with more volatility. After a big jump in 2024, 2025 could see another ~65% revenue increase if it sells more uranium and rare earth carbonate at full-year capacity. Longer-term, if it succeeds in separating rare earths, that could add entirely new revenue lines by 2026–2027. However, because its 2024 base is already higher, the CAGR may moderate compared to the initial jump (e.g. 2021–2024 was exceptional >100% CAGR, 2024–2028 might be more in the 15–25% range annually as operations normalize).

Possible laggards forward: Interestingly, Uranium Royalty Corp may see negative revenue growth in the immediate term. As noted, URC had an outsized revenue in one year from a big uranium sale; with no repeat, its FY2025 revenue is expected to drop ~71%. Over five years, URC’s growth depends on new royalty streams kicking in (e.g. Langer Heinrich royalty from 2024, McArthur River ramp-up). It could see uneven jumps rather than a steady CAGR – lumpy growth tied to project schedules. Companies that remain stuck in permitting or funding challenges might also lag: if, say, a developer fails to advance and remains non-producing by 2030, its revenue will still be negligible. An example could be IsoEnergy if the Anfield assets take longer to restart – it may not generate significant revenue for a few years, making it a growth laggard relative to peers who are already selling product.

🌐 Market Size Estimation: Bear, Base, and Bull Scenarios

Estimating the global uranium upstream market size (in USD) under different scenarios requires assumptions about future uranium demand (volume) and price. Below we outline bear, base, and bull cases with credible sources and reasoning for each:

Bear Case: Low nuclear growth, ample supply – a subdued market. In a bear scenario, nuclear power expansion slows (due to policy setbacks or competition from other energy), and supply is relatively abundant (e.g. idle mines restart easily, secondary supplies remain significant). The World Nuclear Association (WNA) Lower Scenario projects global reactor requirements of only ~107,000 tU by 2040, which is modest growth from ~68,000 tU today. In this case, annual uranium demand might hover around 70,000–80,000 tU through the late 2020s (approximately 155–175 million lbs U₃O₈). With adequate supply, uranium prices could revert to the marginal cost of production. Many analysts cite $40–50/lb as the incentive price for lower-cost projects in oversupplied conditions. For instance, in the mid-2010s bear market, prices fell to ~$20–25/lb, well below sustainable levels, before recovering. In a bear case we assume price stabilizes around $50/lb (enough to keep most existing mines running but little new investment – akin to long-term post-Fukushima lows). Market size calculation: ~165 million lbs/year * $50 = $8.3 billion per year. This would be the rough magnitude in the late 2020s if demand stagnated and prices stayed soft. For a slightly longer-term perspective, using the WNA Lower Scenario 2040 figures: 107,000 tU (~236 million lbs). At $50/lb, that yields ~$11.8 billion annual market size. Thus, bear case market size ≈ $8–12 billion/year (order of magnitude). In this environment, the market value remains similar to or below current levels (today’s market is ~$9–10B at ~150M lbs * $60–$65).

Base Case: Steady growth – tight but balanced market. In the base case, global nuclear capacity grows as currently planned and some new builds occur for climate goals, leading to moderate demand growth, while mining output increases but struggles to fully keep pace initially. The WNA Reference Scenario (2023 report) forecasts uranium requirements rising to ~150,000 tU by 2040 (a ~2.2x increase from 2024). By 2030, WNA projects about 87,000 tU (~191 million lbs) demand – ~28% above 2024 levels. This implies a CAGR of ~4–5% in demand, consistent with many analyses (WNA raised its demand CAGR forecast to 5.3% through 2040). In a base scenario, the market moves into a mild structural deficit (demand > primary supply), which supports higher prices in real terms, but new mines are gradually built to prevent extreme shortages. We might assume long-term contract prices in the $70–$80/lb range – enough to incentivize new production (though some experts argue $80+ is needed for many greenfield projects). Indeed, by mid-2025, term prices have firmed around $70–$80 and spot around $60–$65. For a base case calculation, take ~200 million lbs/year demand at ~$75/lb as a mid/late-2020s average. Market size = 200M lbs * $75 = $15 billion/year. This aligns with other estimates: DataM Intelligence reports the uranium market was ~$9.3B in 2024 and will reach ~$13.6B by 2032 under a moderate growth outlook (implying mid-$70s pricing given volumes). By 2040, using WNA’s 150,000 tU (~330M lbs) and a perhaps slightly higher price of ~$80, the market would be ~$26 billion. To be conservative, we can say base case ~ $15–25 billion annually in the 2030s, with mid/late-2020s around the lower end of that range (low teens in $billions).

Bull Case: Nuclear renaissance – undersupply drives a booming market. The bull scenario envisions rapid nuclear power expansion (far exceeding current plans) coupled with supply shortfalls due to years of underinvestment and possible geopolitical supply disruptions. The WNA Upper Scenario sees uranium demand exceeding 204,000 tU by 2040. The IAEA similarly has a high case of ~100,000 tU/year by 2040 (nearly double current levels), which implies ~4–5% annual growth sustained over two decades. In a bull case, by the early 2030s demand could easily surpass 100,000 tU (~220 million lbs) annually. Supply would struggle to ramp up – many new mines would be required, and any delays or shortfalls could lead to a prolonged supply deficit. This is the scenario where uranium prices spike to incentive levels and beyond. For instance, Citi’s bull-case forecast (as of Sep 2025) has uranium reaching $125/lb in the near term. In a sustained bull market, prices could remain well above $100 if shortages persist. A conceivable bull scenario by ~2030: demand ~230–250 million lbs, and price in the $100–$120/lb range. Market size = 240M lbs * $110 ≈ $26.4 billion/year. If the tightness is extreme (some predict possible spikes to $150+ if utilities scramble), the market value could temporarily exceed $30–40B, but using a more sustainable high price: e.g. at WNA Upper 2040 demand of ~450M lbs, even at $100/lb, that’s $45 billion annually. For an upper-bound, using Citi’s $125/lb and ~450M lbs (assuming nuclear growth truly accelerates to meet climate goals), yields ~$56 billion. Realistically, a bull case through 2030s might see the market size doubling or tripling from current levels. We can bracket bull case as $25–50 billion per year in the 2030 timeframe (with the lower end assuming just moderately higher prices around $90–100 and some volume growth, and the upper end assuming both strong volume and price well into triple digits).

📊 Major Industry Trends and Growth Drivers

Several powerful trends and long-term drivers are shaping the global uranium upstream industry. These trends underpin optimistic demand forecasts and are driving strategic shifts among companies and governments:

Resurgence of Nuclear Energy for Climate and Energy Security: After a post-2011 lull, nuclear power is experiencing a policy and public opinion turnaround. Governments worldwide are prioritizing nuclear for decarbonization and energy security, which directly boosts uranium demand. At COP28 (2023), 20+ countries (including the U.S.) committed to tripling nuclear capacity by 2050 as part of climate action. Major economies like China, India, and the U.S. have ambitious reactor build programs, while countries that once planned phase-outs (Japan, South Korea, France) have extended reactor lifetimes or added new projects. The result is an expected 28% surge in uranium demand by 2030 and more than doubling by 2040 under WNA’s latest outlook. This growth is a structural driver: more reactors (and life extensions) mean higher baseline uranium requirements for decades. Climate change objectives (net-zero pledges) are giving nuclear a prominent role due to its low carbon footprint, and geopolitical tensions (e.g. reliance on Russian gas) have underscored nuclear’s value for energy independence. This has led to stronger political support and new government initiatives: e.g. the U.S. ADVANCE Act streamlining reactor licensing, France reversing course to build new reactors, the EU including nuclear in its green taxonomy, etc. In sum, a broad pro-nuclear policy environment is a key trend driving a structural upswing in uranium demand long-term.

Small Modular Reactors (SMRs) and Advanced Reactors: Technological innovation in reactor design is another growth vector. SMRs and advanced reactors are moving from concept to reality, promising to open new markets and applications for nuclear. These smaller units (typically <300 MWe) feature lower upfront costs, factory fabrication, and enhanced safety, making nuclear more accessible beyond big utilities. Several SMR designs have achieved regulatory approvals by 2025 and are slated for deployment in the next 5–10 years. Countries like Canada, U.S., UK, and Poland have SMR projects in pipeline. SMRs could power remote communities, industrial sites, or replace coal plants, expanding nuclear’s footprint. Importantly for the uranium industry, many advanced reactors (especially Gen IV designs) require High-Assay Low-Enriched Uranium (HALEU) fuel (up to 20% U-235), which could increase uranium demand per reactor (due to lower burn-up efficiency initially) and create new value-added demand for enrichment services. SMRs also have shorter refueling cycles in some cases, meaning fuel throughput might increase. While still early, the potential mass deployment of SMRs in the 2030s is a bullish demand driver: it’s cited as one reason WNA raised its demand growth forecast from 4.1% to 5.3% CAGR through 2040. Additionally, advanced reactor programs (like TerraPower’s Natrium, X-energy’s Xe-100) have spurred western governments (U.S., Canada) to invest in HALEU production (benefiting companies like Centrus). The SMR trend thus drives both higher uranium volume needs in the long run and shifts in the fuel cycle (more enrichment and specialized fuel fabrication).

New Uses of Nuclear Power (Beyond Traditional Grid Electricity): An emerging trend is nuclear power being considered for non-electric applications, which indirectly boosts uranium demand. For example, the explosion of energy-intensive computing (AI and big data) has tech giants exploring nuclear to power data centers. Microsoft, Google, Amazon, and Meta have all announced initiatives to incorporate nuclear energy for their growing electricity loads. This digital economy linkage could add meaningful reactor demand beyond public utilities. Likewise, nuclear is being eyed for green hydrogen production via electrolysis (providing constant clean power to make hydrogen), for process heat in industrial applications, for desalination, and for district heating in colder climates. Each of these uses could add to reactor build totals or capacity factors. For instance, high-temperature reactors dedicated to hydrogen production or industrial heat could become a niche but significant segment by 2030s. While these are in early stages, they form part of the narrative that nuclear is broadening its value proposition, creating additional sources of uranium demand beyond just grid electricity.

Supply Constraints and Underinvestment: On the supply side, a critical trend is the lasting impact of a decade of underinvestment in uranium mining. From 2013–2017, uranium prices languished around $20–$30/lb, causing many mines to close and exploration spending to collapse. The World Nuclear Association notes that as of 2022, 78% of reactor requirements came from primary production (up from ~60% a few years prior), meaning secondary supplies (stockpiles) have been drawn down heavily. Many mines were depleted or suspended, and very few new projects were developed in the 2010s. Now, even as demand rises, the pipeline of new mines is thin. WNA’s latest Fuel Report warns that existing mine output will fall off sharply by mid-2030s – roughly half of current production capacity may end by 2040 as major deposits are exhausted. Indeed, by 2030, some large sources like Cigar Lake may wind down unless expanded. This sets the stage for a potential structural supply gap. The industry will need to double primary production by 2040 in the upper-demand scenario, requiring many new mines. However, new projects face long lead times (often 7–10 years from discovery to production), so the response is inherently slow. This dynamic (rising demand vs. slow supply response) is a key driver of the current uranium bull market. It has already led to prices climbing from ~$20 in 2017 to ~$70 in 2025. As one industry CEO summarized: “Supply and demand fundamentals suggest the uranium price has to increase substantially… it’s very hard to bring on new supply in time”. The trend of persistently tight supply is further exacerbated by events like COVID-19 disruptions (which briefly removed ~20% of global supply in 2020) and currently by supply chain issues (e.g. acid shortages in Kazakhstan). Combined, these factors serve as a long-term driver for higher prices and incentivize new entrants – but until those mines materialize, existing producers benefit from a seller’s market. In short, the legacy of underinvestment has created a classic commodity upswing backdrop: demand rising into a supply-constrained market, fueling a multi-year bull trend.

Geopolitical Realignment of Uranium Supply Chains: Geopolitics is increasingly influencing where uranium is sourced and how nuclear fuel is procured. A major trend is the effort by Western countries to reduce dependence on Russian nuclear services (conversion, enrichment) and, to some extent, on Kazakh/Uzbek uranium which is exported via Russia. Russia’s war in Ukraine in 2022 spurred calls for embargoing Russian uranium (the U.S. is considering bans on Russian enrichment, the EU and others have discussed reducing imports). Meanwhile, Kazatomprom (Kazakhstan) still supplies 40% of world uranium, but ~50% of Kazakh output currently goes to China, and Kazakh exports to the West rely on transit routes that avoid Russia (a logistic challenge). This East-West bifurcation is prompting western utilities to diversify supply contracts towards non-Russian sources. It’s also driving government support for domestic production in friendly jurisdictions: e.g. the U.S. government’s uranium reserve purchase (buying from U.S. mines), Canada’s inclusion of nuclear in clean investment plans, and potential collaborative stockpiling among allies. One concrete result: Western investment in enrichment capacity – e.g. Urenco in the UK/U.S. expanding, and the DOE funding Centrus – because currently Russia’s Rosatom controls nearly half of global enrichment and much of the conversion capacity. Geopolitics is thus a driver for new upstream investments: friendly-nation uranium projects (in Canada, Australia, Namibia, etc.) are more likely to get fast-tracked and financed due to this security premium. It’s also leading to trade and tariff considerations (the U.S. has discussed re-imposing the Russian suspension agreement limits more stringently). In sum, security of supply is now a key theme, where not all uranium is seen as equal – origin matters. This trend benefits non-Russian producers and is a growth catalyst for projects in stable jurisdictions as utilities re-balance their portfolios. The WNA notes that geopolitical shifts since 2022 are “shaping both global demand for nuclear energy and availability of fuel cycle services” and call for “timely investment” in all fuel supply stages to ensure security.

Financialization of Uranium Markets: In recent years, uranium has seen an influx of financial players and vehicles that are changing market dynamics. The launch of physical uranium investment funds like the Sprott Physical Uranium Trust (SPUT) and Yellow Cake plc is a notable trend. These entities buy and hold physical U₃O₈, taking supply off the market to offer investors direct exposure to uranium price upside. SPUT alone purchased millions of pounds in 2021–2022, contributing to price increases. Such financial demand effectively functions as a new category of demand (neither reactor nor government, but investor-driven). ETFs and specialty funds have also grown – e.g. URNM and URNJ (uranium mining ETFs) have channeled capital into the equities. This increased liquidity and speculative interest can amplify price moves. For instance, spot price volatility in 2021–2022 (when uranium jumped from ~$30 to ~$50+) was partly attributed to these funds aggressively sequestering uranium. The trend continues, with more institutions warming up to uranium as a long-term clean energy play. Additionally, trading volumes and market efficiency have improved – spot market now accounts for ~25% of transactions (up from <15% years ago) and serves as a reference for many term contracts. More active trading and transparency in price discovery (via brokers, price reporting) have made the uranium market more accessible. Overall, financialization has provided miners alternative funding avenues (e.g. selling to Yellow Cake or SPUT for immediate cash) and contributed to a more robust pricing environment. However, it also means higher volatility, as seen in 2022–2023 when prices ran up quickly to ~$60+ and had periodic pullbacks. On balance, this trend supports higher long-term prices by locking away inventories (SPUT+Yellow Cake hold >70 million lbs combined), thereby tightening supply-demand balance.

Innovation in Mining & Milling – Environmental Focus: Technological and environmental trends within the industry are shaping how uranium will be produced:

The continued shift toward In-Situ Recovery (ISR) mining is notable. ISR now accounts for about 50% of world uranium production (mostly in Kazakhstan, Uzbekistan, and USA). ISR mines have a smaller surface footprint and can be developed in modular fashion. They often have lower operating costs and shorter lead times than conventional mines. As environmental regulations tighten, ISR (which avoids open pits or large tailings piles) is increasingly favored when geology permits. For example, companies like Denison are innovating by applying ISR to high-grade sandstone deposits (traditionally mined via underground methods). If successful, this could unlock lower-impact mining of deposits that would otherwise face local opposition due to water use or waste.

There’s also focus on milling innovation and waste handling – e.g. using existing mills (like White Mesa, Shootaring) to process ore from various small mines, reducing the need for new milling infrastructure. Heap leaching for low-grade resources, more efficient tailings management, and deployment of remote monitoring and automation (as Cameco did during McArthur River’s care-and-maintenance upgrades) are improving safety and lowering costs.

On the ESG front, uranium mining is striving to clean up its image. This includes better engagement with Indigenous communities (e.g. Energy Fuels negotiating with Navajo Nation for ore transportans.org, Canadian firms partnering with First Nations on project equity), improved remediation plans, and highlighting nuclear’s role in climate change mitigation to counter anti-uranium sentiment. The industry is marketing that “new methods are much cleaner than past practices” – notably the dominance of ISR (which leaves 70% of radioactivity in-ground and uses far less surface disturbance) as evidence.

Another angle is secondary supply innovation: efforts to re-enrich tails (depleted UF₆) or recycle uranium from spent fuel could marginally contribute. Russia has done tails re-enrichment for years; now Orano and others are looking at it again given high prices. It won’t replace primary mining but can add flexibility.

🎯 Key Success Factors and Profitability Drivers

The profitability of uranium upstream companies is driven by a combination of market factors and project-specific attributes. Key drivers include:

Uranium Price Realizations: The single biggest lever for profitability is the market price of uranium (U₃O₈) relative to production costs. Uranium price swings directly affect miner margins – when prices are high, even relatively high-cost mines become profitable; when prices fall below cost, mines quickly flip to losses. After Fukushima (2011), prices dropped >70% to ~$20/lb, forcing widespread losses and mine closures. Now with prices in the $60–$70/lb range, many operations have moved into the black. For example, Cameco’s average realized price jumped from $43/lb in 2017 to ~$79.70/lb in 2024, boosting its gross profit accordingly. Profitability is highly sensitive to price because uranium mining has a high fixed-cost component – once a mine is running, cash costs per pound may be $20–30, so each additional dollar on the sales price largely flows to the bottom line. Many new projects, however, require prices in the $50–$70+ per lb range to be viable (to cover full costs including capital). Industry experts estimate incentive prices above ~$95–$100/lb are needed to bring significant new greenfield production online. Thus, current producers with existing assets enjoy a cost advantage and strong margins at today’s ~$70/lb (since most operating mines have AISC well below $70).

Ore Grade and Deposit Type (Cost of Production): The cost structure of a uranium mine is primarily determined by the ore grade, mineralogy, and mining method. High-grade deposits (like those in Athabasca with 1%–20% U₃O₈) allow far more uranium to be extracted per ton of rock, drastically lowering per-pound costs – these mines tend to be extremely profitable when operating. For instance, Cameco’s McArthur River and Cigar Lake, with grades 50–100x the world average, have operating costs reportedly in the lowest quartile (historically <$20/lb). In contrast, low-grade mines (e.g. 0.01%–0.05% U) must move huge tonnages, raising costs. This is why Kazakh ISR mines (low grade ~0.05% but ISR method is cheap) and Athabasca mines (very high grade ~5–20%) are among the most profitable sources. The mining method is also critical: In-Situ Recovery (ISR) tends to have lower operating and capital costs than conventional mining. ISR avoids drilling, blasting, and milling of large rock volumes – instead, solution is circulated underground to dissolve uranium. According to WNA/TradeTech data, ISR mines often have lower C1 cash costs, and while they have ongoing wellfield capital, they can achieve low fully-loaded costs if resources are amenable. For example, Kazatomprom’s ISR operations in Kazakhstan produce profitably at ~$20–$30/lb all-in cost, which was still above spot in the 2010s but now yields solid margins. Conversely, conventional underground or open-pit mines with difficult metallurgy or deep ore (e.g. some projects in Africa or low-grade U.S. conventional mines) might have breakeven costs in the $60–$80 range, making them marginal unless prices are high. To break it down:

Grade: higher grade = fewer tonnes to mine per lb of U = lower cost per lb.

Depth and geology: shallow deposits or those in permeable sandstone (ISR-suitable) are cheaper; deep hard-rock deposits need shafts, etc., raising capital and operating costs.

Mining method: ISR (or heap leach) vs. underground vs. open-pit – each has different cost profiles. Open pits remove a lot of waste (high stripping) but are simpler operations; underground has less surface disturbance but higher labor and technical demands. ISR has high upfront wellfield capital but then relatively steady low operating cost (mostly acid, pumps, etc.). Trade-offs are seen in the cost structure: for ISR, only ~25–30% of lifecycle cost is operating cash cost, ~50% is upfront and sustaining capital, whereas for open-pit mines ~70% of cost is operating cost and ~20% capital. This means ISR profitability can be sensitive to ongoing wellfield investment but generally benefits from low variable cost, whereas conventional mine profitability is more sensitive to day-to-day operating efficiency.

Scale and Capacity Utilization: Mining is subject to economies of scale. Larger operations that can achieve high throughput and spread fixed costs over more pounds tend to have better unit economics. For example, a mill processing 3,000 tonnes/day vs. 300 t/day will have much lower cost per ton processed. Cameco’s McArthur/Key Lake operation benefited from scale (producing 18 Mlbs/year at its peak), which lowered its unit costs significantly. Conversely, small-scale mines (like boutique U.S. conventional mines producing <0.5 Mlbs/year) often struggle with high unit costs because fixed expenses (regulatory, overhead, milling) are supported by few pounds. Running assets at high utilization also improves profitability – e.g. when Cameco idled McArthur River 2018–2022, costs accrued without revenue, hitting margins; now at full run-rate, profitability returned. Similarly, Ur-Energy’s Lost Creek operating at only a trickle for years had negative gross margins, but as it ramps up production toward capacity, unit costs drop and margins improve. Capacity utilization is a key near-term profitability lever: e.g. Energy Fuels in 2024 used White Mesa Mill for both uranium and rare earths, increasing utilization which helped cover fixed costs, thereby improving margins on both products. In sum, bigger and fuller operations = lower cost per lb = higher profits.

Contract Portfolio and Pricing Strategy: How a company sells its uranium significantly impacts realized price and thus profitability. Companies with favorable long-term contracts (i.e. at prices above spot during downturns) maintained profitability better in the 2010s. For example, Cameco had legacy contracts in the ~$50s per lb during the 2016–2019 period when spot was $25–$30, allowing it to stay cash-flow positive. By 2024, Cameco’s newer contracts included market-related pricing which benefited from the price upswing. The mix of fixed vs. market-based contracts, contract durations, and customer portfolio all matter:

Downside protection vs. upside exposure: A company heavily hedged at low fixed prices could miss out on a bull market (hurting short-term profitability). Conversely, too much spot exposure in a weak market hurts margins. Striking the right balance is key. Cameco, for instance, now seeks market-linked contracts with floors – this way they ensure a minimum profitable price, but also get upside if market rises. That approach smooths profitability over cycles.

Creditworthiness of buyers and contract performance: Utilities are generally reliable buyers, so contract default risk is low. But one must consider delivery obligations – if a miner has contracted more than it can produce (especially juniors signing contracts), it might have to buy in the market to deliver if production falters, potentially at a loss. Keeping contracts aligned with production capability avoids that.

Conversion & enrichment components: Sometimes miners sell UF₆ (enriched product) or partner to include conversion in the sale. For instance, companies that can offer an integrated fuel bundle might command better pricing. But pure upstream usually sells U₃O₈. Centrus, on the other hand, profits from SWU (separative work unit) prices in enrichment contracts. Its profitability depends on the spread between SWU price and its cost. Currently, enrichment prices have surged (Western SWU > $150/SWU in 2023 from ~$60 a few years ago) due to Russian supply concerns, benefiting enrichers. This is analogous to uranium price for miners – a key driver for Centrus is SWU market rate. In 2022–2023, Centrus enjoyed a lucrative DOE contract that paid for HALEU production, directly boosting its marginsans.org. So for fuel service providers, their “commodity price” is the service fee (SWU, conversion price). High utilization of their enrichment capacity also lowers unit cost (Centrus running its AC100s at capacity yields lower per-SWU cost).

Operating Efficiency and Cost Management: Within any given mine’s control, efficient operations drive profitability. This includes:

Cost control on inputs: Uranium mining uses reagents (acid, peroxide), electricity, diesel, and labor. Managing these costs (through bulk procurement, local sourcing, or process optimization) can improve margins. For instance, Kazakhstan’s ISR mines faced a constraint with sulfuric acid supply in 2022–2023; acid shortages limited production. When acid prices spiked, it pressured costs. Companies that invest in securing supplies (Kazatomprom built its own acid plant) or improving acid utilization have an edge.

Labor and productivity: Skilled labor is needed for safe operations. In some regions (e.g. remote Canadian north or Australian outback), labor is costly and fly-in-fly-out. Automation (use of tele-remote mining at Cigar Lake for example) can improve productivity and reduce labor cost per lb. Safety and environmental compliance are also crucial – poor safety can lead to shutdowns or fines, which hurt profitability. The best operators avoid costly incidents by maintaining high standards.

Recovery rates and grades vs. plan: In mining, actual recovered grade vs. expected grade affects output. If a mill recovers 90% of uranium in ore vs. a planned 95%, that’s a 5% revenue hit. Continuous improvements (better ore blending, improved leaching chemistry) can raise recoveries. Denison’s field tests indicated ~97% recovery of uranium in ISR leach trials – if that can be replicated at scale, it maximizes revenue per amount of resource, boosting project NPV and margins. Essentially, technical optimization (recovery, throughput, equipment reliability) directly drives cost per lb.

Royalties and taxes: The take by governments varies widely. Profitability for miners in high-royalty regimes (e.g. some jurisdictions have 5–10% gross royalties plus corporate tax) is lower than in places with minimal royalties. For example, Uranium Energy Corp operates in U.S. states with royalty burdens (Texas has ~8.25% severance tax equivalent; Wyoming around 4% severance + federal royalty on federal leases). Cameco in Canada pays provincial royalties that escalate with price. These extrinsic costs affect net margins per lb.

Economies of scope: Companies like Cameco and Orano that have conversion facilities or fuel fabrication can sometimes capture more value (conversion prices have soared recently to ~$30/kgU from <$10 a few years ago, benefiting those with conversion capacity). Cameco’s fuel services division significantly added to earnings in 2024 (division revenue C$459M) and enjoyed an 88% jump in Q1 2025 due to higher conversion prices. This vertical integration provided an additional profitability lever beyond mining.

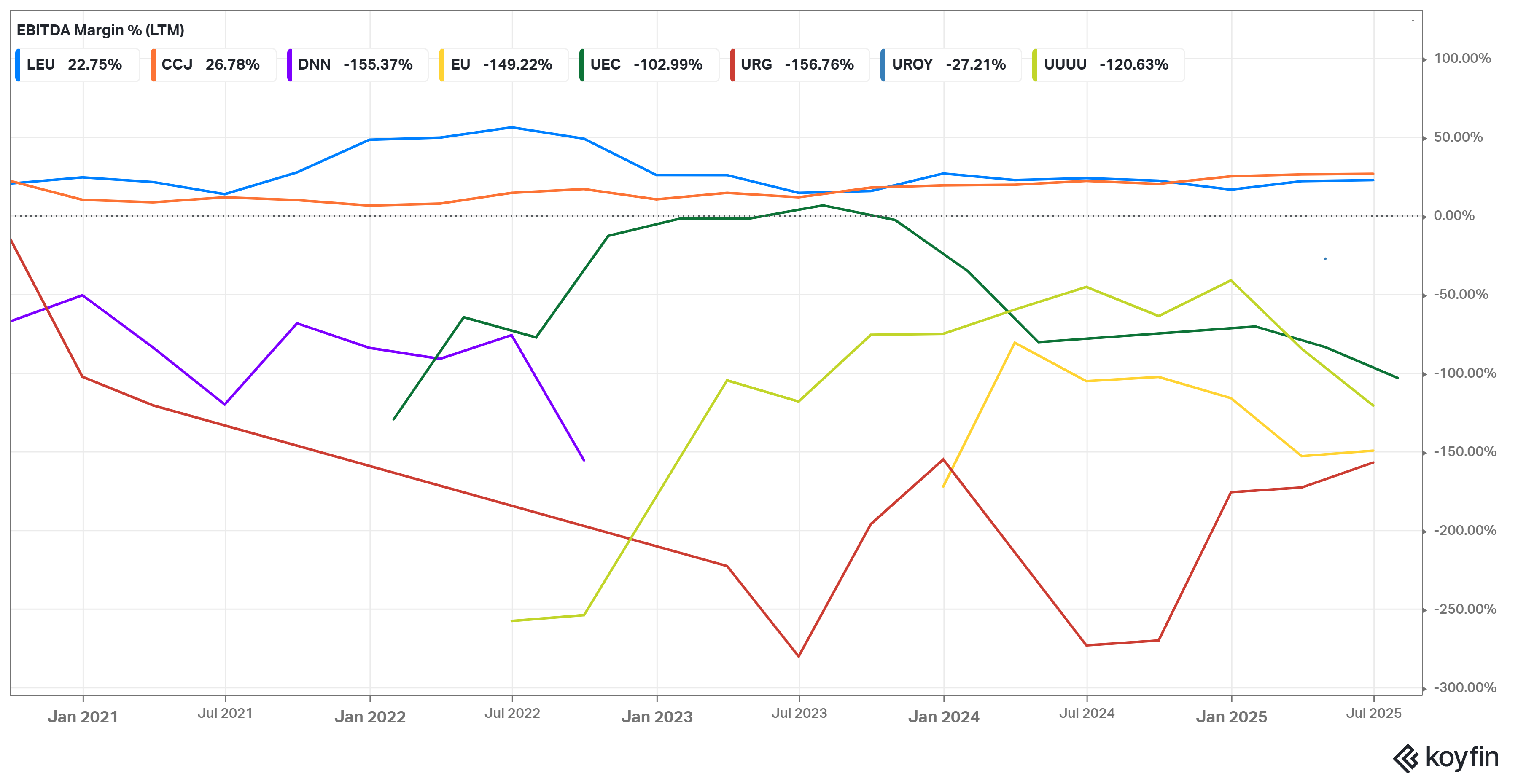

Project Stage and Capital Efficiency: It’s worth noting that developers vs. producers face different “profitability” considerations. Developers (NexGen, Denison) currently have negative earnings and cash flow (e.g. Denison’s EBITDA margin was ~-155%) because they are spending on exploration and studies with no revenue. Their “profitability” will come only once mines are built. So for them, a key driver is access to low-cost capital – if they can finance development cheaply (through strategic investors, farm-outs, etc.), they preserve future project IRR. Companies that manage to fund construction without excessive dilution or high debt costs will deliver higher eventual per-share earnings (a win for shareholders).

Also, timing of project execution matters – building a mine on budget and on schedule ensures that capital costs don’t spiral and that the mine can catch favorable market conditions. For instance, Paladin’s Langer Heinrich restart was timed to complete in 2024 when prices are high, which will likely yield strong early cash flows to payback investment.

Primary Fuel Cycle Cost Drivers: In enrichment (for Centrus), profitability drivers include:

SWU price (as noted),

Centrifuge efficiency and output: how many SWU per machine and energy cost per SWU. If Centrus can improve its centrifuge output or get cheap power, it improves margins.

Government support: Centrus’ HALEU contract is cost-plus; DOE covers a portion of costs, effectively guaranteeing a profit. Extension of such contracts or additional government incentives for domestic enrichment (which are likely given geopolitical aims) directly boost Centrus’ bottom line.

Utilization of enrichment capacity: If Centrus can fill its cascade with commercial work after the DOE demo, each additional SWU sold spreads fixed costs (facility overhead) and increases profit per unit.

Exchange Rates: Many uranium producers incur costs in local currency but sell uranium in USD (the global pricing currency). For example, Cameco’s mines are in Canada (costs in CAD) but sales in USD; Kazatomprom costs are in Kazakhstani Tenge, sales in USD. A weak local currency vs. USD reduces costs in USD terms, boosting profit. In recent years, a strong US dollar has benefited Canadian producers – Cameco noted that a weakening CAD (vs. USD) added to its realized price advantage in 2025. Conversely, currency appreciation can hurt. Thus, macro forex trends can be a subtle profitability driver for multi-national producers.

In practical terms, this is why Cameco and Kazatomprom are very profitable at $60–$70/lb, why many U.S. juniors needed ~$70+ to restart (and are only now turning cash-flow positive), and why developers push for financing when prices approach incentive levels. It also explains company behavior: e.g. Cameco’s willingness to cut production in 2018 was a bet on price as the main profit driver (foregoing volume at unprofitable prices to support a future with higher prices). Now that prices have improved, profit drivers are aligned and those cuts have paid off in the form of a tighter market and higher margins for all producers.

💼 Porter’s Five Forces Analysis

1. Threat of New Entrants – Moderate to Low.

Barriers to entering uranium mining are fairly high due to the specialized nature of the industry:

Resource Availability & Exploration Barrier: Viable uranium deposits are geologically scarce and often already controlled by existing companies or state entities. Discovering a new significant deposit requires substantial exploration investment and luck. Most new entrants cannot easily “find” a world-class deposit – the low-hanging fruit has largely been found (e.g. Athabasca giants, Kazakh ISR fields, etc.). Additionally, acquiring known deposits through M&A is capital-intensive.

Capital Intensity: Developing a uranium mine (especially conventional underground or open-pit) is extremely capital-intensive – often hundreds of millions to over a billion USD for large projects (e.g. NexGen’s Arrow FS is ~$1.3B capex). ISR mines are cheaper but still require tens of millions and technical know-how. New entrants without deep financial backing face a steep hurdle. Financing can be challenging given uranium’s historical price volatility and the long lead times (investors must wait years for returns). Only during strong uranium bull markets do capital markets open up enough to fund many newcomers (e.g. mid-2000s saw a wave of juniors, many of which later vanished when prices fell).

Regulatory and Technical Barriers: Uranium mining is heavily regulated due to radiation and environmental concerns. Permitting a new mine can take years – e.g. in the U.S., obtaining all necessary permits has stretched close to a decade for some projects due to public opposition and rigorous environmental reviews. For instance, Canada’s regulatory process and community consultations add time and complexity (though Canada is mining-friendly, it’s still rigorous). In the U.S., uranium projects face opposition for environmental reasons (e.g. Virginia’s uranium mining ban, ongoing challenges in Arizona near the Grand Canyon). These factors discourage casual new entrants. Nuclear regulatory experience and a strong safety culture are needed to operate – not easily acquired by newcomers.

Economies of Scale and Experience: Incumbents like Cameco, Orano, and Kazatomprom have decades of experience, established teams, and existing infrastructure (mills, conversion facilities, logistics) which give them cost and speed advantages. New entrants starting from scratch must often partner with experienced firms (or hire their expertise) to overcome the steep learning curve of handling radioactive material and complex hydrometallurgy.

Market Barriers (Customers and Contracts): Utilities typically prefer to buy from proven producers with reliable track records. A new entrant without a production history might struggle to secure long-term contracts initially, forcing them to sell into the spot market – a risky proposition that can deter project financing. Establishing relationships with utility buyers and qualifying as an approved supplier (utilities do due diligence on producers’ sustainability and capabilities) raises the bar for entry.