Offshore / Marine Services Industry - USA

Positioned for Cyclical Upside Amid Tightening Capacity and Rising Energy Investment

The Offshore / Marine Services industry comprises companies that support offshore energy exploration and production through specialized maritime and logistics services. These firms provide the transportation of personnel and supplies between onshore bases and offshore installations using vessels and aircraft, as well as a wide range of subsea engineering and field support services. For example, offshore support vessel (OSV) operators run fleets of ships that deliver equipment, drilling mud, and consumables to rigs and platforms, ferry crews, and sometimes serve as floating accommodations or emergency response units. Helicopter service providers play a complementary role by flying workers to offshore rigs and performing search-and-rescue (SAR) missions in remote ocean areas. In addition, several companies offer subsea inspection, maintenance, and engineering services – deploying remotely operated vehicles (ROVs) and dive teams to install or repair undersea infrastructure, and conducting specialized operations like well intervention and decommissioning of old wells. In short, the industry produces the critical marine and logistical support that enables offshore oil & gas projects (and increasingly offshore wind farms) to operate efficiently and safely, from initial exploration through development and eventually decommissioning.

🏭 Key Companies

Key publicly listed players based in the U.S. include a mix of vessel operators, aviation providers, and subsea service specialists. The most relevant companies (and their primary focus areas) are:

Bristow Group Inc. (VTOL) – A leading provider of offshore helicopter transportation services. Bristow ferries personnel to offshore oil and gas installations and performs SAR and support missions for government and civil organizations. It operates a large fleet of heavy and medium helicopters adapted for marine environments.

TechnipFMC plc (FTI) – A global subsea engineering and services company that provides technologically advanced systems for offshore oil & gas development. TechnipFMC is a leader in subsea production equipment (like underwater trees, flowlines, and control systems) and offers fully integrated project services (iEPCI) from design and manufacturing to installation and commissioning. Its engineering and manufacturing capabilities make it a critical partner for offshore field development, linking the wellhead on the seafloor to surface facilities.

Helix Energy Solutions Group (HLX) – A niche offshore services contractor specializing in subsea well intervention, robotics, and decommissioning. Helix operates specialized vessels that can enter subsea wells to perform maintenance, repairs, or plug and abandonment of depleted wells. The company prides itself on these production-related services and its fleet of intervention vessels and ROVs, which provide cost-effective alternatives to drilling rigs for well work.

Oceaneering International (OII) – A diversified subsea engineering and applied technology company based in Houston. Oceaneering is the world’s largest operator of ROVs, which are used for inspection, repair, and maintenance of offshore infrastructure. It also provides specialty subsea hardware, deepwater installation support, manned diving services, and survey/mapping services for offshore energy projects. Oceaneering also leverages its remote robotics expertise in adjacent markets like defense and aerospace, though offshore oil & gas remains a core business.

Tidewater Inc. (TDW) – The world’s largest operator of offshore support vessels, supplying marine logistics to the global offshore energy industry. Tidewater’s fleet of platform supply vessels (PSVs), anchor-handling tugs, and other workboats serves offshore drilling rigs and production platforms worldwide. Having survived a major downturn and consolidated competitors, Tidewater has extensive global reach across all major offshore regions and focuses on high utilization and efficient operations of its vessels.

SEACOR Marine Holdings (SMHI) – A U.S.-based OSV provider with a technically advanced, fuel-efficient fleet. SEACOR Marine offers a “complete suite of transport services” for offshore energy, including crew transport, cargo supply, and accommodation support, with operations spanning five continents. It has also expanded into servicing offshore wind projects. SMHI is smaller in scale than Tidewater, but emphasizes modern, environmentally friendly vessels (it recently ordered new battery-hybrid PSVs) to carve out a competitive edge.

These six companies form the core of the U.S.-domiciled offshore/marine services public market. We exclude other oilfield service firms that are not focused on marine/offshore support – for instance, drilling contractors like Transocean or Nabors (which provide rigs, not support services), and integrated oilfield service giants like Schlumberger or Halliburton (which do include offshore work but are diversified across onshore and other segments). We also omit foreign-based offshore contractors (e.g. Norway’s DOF Group or UK’s Subsea7) since the focus is on U.S.-listed and domiciled players. The selected companies represent the primary publicly traded U.S. players dedicated to offshore logistics, aviation, and subsea services.

🎢 Historical and Forecasted Growth

After a brutal downturn in the mid-2010s followed by the COVID-19 slump in 2020, the offshore services industry entered a strong recovery phase in 2022–2024, with many companies returning to growth as offshore drilling and project development rebounded. The table below summarizes recent revenue growth rates for the key companies, including the latest year-over-year (YoY) growth, forward expected growth, and 3- and 5-year compound annual growth rates (CAGR):

Several clear patterns emerge from these figures. Tidewater (TDW) is the standout growth leader – it achieved 33% revenue growth in the most recent year and is expected to grow another ~13% forward, giving it by far the highest 3-year CAGR (over 53%). This reflects the OSV sector’s sharp rebound: Tidewater, having restructured and consolidated competitors, was positioned to capitalize on surging vessel demand and day rates. In 2024, Tidewater’s revenues reached $1.36 billion – an increase of 33.3% over 2023 – driven by higher average day rates (up 27% YoY) and improving vessel utilization. That growth far outpaced most peers. Helix (HLX) also shows a high multi-year CAGR (26.5% over 3 years), but its most recent growth has stalled (~0% in 2024). Helix’s spike was partly due to expansion into new services (e.g. its 2022 acquisition of Alliance in the Gulf of Mexico) and a post-COVID demand bounce for well intervention, but recent results have been flat as certain projects were delayed and its legacy businesses faced headwinds.

TechnipFMC (FTI) demonstrates solid and steady growth: ~14% revenue gain last year and similar ~10% expected forward. Its three-year CAGR ~13.7% is healthy, though the five-year CAGR is –5% due to a earlier revenue drop around 2019–2020 (TechnipFMC underwent a major reorganization, including spinning off its onshore construction division in 2021, which reduced its top-line baseline). Now, however, FTI is firmly on an upswing – its subsea equipment and services orders surged in 2023 (inbound orders $9.7 billion, +45% YoY) pushing backlog to $13.2 billion (+41%), which bodes well for future revenue growth. Oceaneering (OII) has been a moderate grower – ~10% in 2024 and mid-single-digit projected going forward – resulting in a 5-year CAGR of ~5.5%. Oceaneering’s growth is constrained relative to more pure-play oil service firms because a portion of its business is in stable, non-oil sectors (like defense robotics), and it did not see as dramatic a downturn or upturn as the vessel providers. Still, OII’s steady growth reflects consistent demand for ROV services and subsea products as offshore activity gradually increases.

On the low end, SEACOR Marine (SMHI) actually saw a revenue decline of 6% in the last year, and essentially flat sales expected in the near term (~0.3% forward). This makes SMHI a growth laggard – despite a respectable 5-year CAGR ~9.8% (coming off a very low base in the late 2010s), its recovery has been uneven. SMHI had significant idle capacity and disposed of some older vessels, which, combined with operational challenges, led to shrinking revenue in 2024. Bristow (VTOL) has maintained modest single-digit growth (around 9% YoY and forward). As a helicopter service provider, Bristow’s revenues are often tied to long-term contracts (for oil companies or government SAR services), yielding more stable but lower growth than the highly cyclical marine vessel segment. Bristow’s post-2020 reincarnation (after merging with Era Group) means long-term CAGR figures aren’t available, but its growth trajectory is relatively flat compared to the high-flying OSV segment.

In summary, the industry’s growth profile in recent years has been strong overall, with a clear bifurcation: marine vessel-focused companies (like Tidewater) are leading the pack as offshore drilling activity roars back, while others are growing more moderately or stabilizing. The forward outlook (as of early 2025) suggests growth may temper from the breakneck pace of 2022–24 but remain positive, supported by hefty backlogs (FTI), high vessel utilization (TDW), and selective expansion opportunities. The leaders in top-line expansion – Tidewater in particular – reflect the robust recovery in offshore logistics demand, whereas laggards like SMHI indicate that not all players have benefitted equally (smaller firms may still be catching up or reorganizing). Overall, the industry is emerging from its downturn with significant momentum heading into 2025, albeit with growth rates likely normalizing as the rebound matures.

📈 Industry Trends and Growth Drivers

Several macro trends and sector-specific drivers are shaping the offshore/marine services industry’s current growth phase and future outlook:

Offshore Drilling Rebound & High Utilization: A sustained recovery in offshore exploration and drilling is the fundamental driver lifting the entire marine services sector. Global offshore rig activity has risen significantly – by late 2024, marketed offshore rig utilization reached about 87%, the highest since 2016. This rebound has directly increased demand for support vessels and services. OSV fleet utilization hit ~75% in 2024 and could rise further in coming years, indicating a tightening market. As drilling rigs reactivate or new ones are deployed, they require more supply runs, crew transfers, ROV services, and well interventions – a positive demand shock for all service providers. Higher day-rates and pricing power have followed: for example, Tidewater’s average vessel day-rate jumped to ~$21,300 in 2024 (up 26% YoY), and was still climbing quarter by quarter. This upcycle in offshore oil & gas activity is underpinned by oil prices stabilizing at healthy levels (generally $75–$90/bbl through 2024) and renewed confidence among E&P companies to sanction offshore projects.

Surging Upstream Investment & Project Sanctions: After years of underinvestment, oil companies significantly increased capital expenditures in offshore developments. Global upstream engineering, procurement, and construction (EPC) spending was projected around $63 billion in 2024, up 43% year-on-year. This wave of investment is filling the order books of subsea equipment and service firms. TechnipFMC, for instance, has reported record inbound orders and backlog thanks to a rush of new deepwater projects (its subsea order backlog grew 50% in 2023 to over $12 billion). Regionally, big offshore developments in Latin America (Brazil and Guyana), the Middle East (huge gas projects), and Southeast Asia are leading the charge. These multi-year projects drive demand not only for hardware (subsea trees, pipelines) but also for installation vessels, construction support, and ongoing maintenance services. Essentially, an offshore capex boom is underway, which directly translates to more work for marine service contractors in the form of new contract awards, longer project backlogs, and higher utilization of assets.

Offshore Wind Expansion and Energy Transition: The push for renewable energy, especially offshore wind power, is emerging as a new growth avenue for marine service companies. Many OSV operators are finding opportunities in offshore wind farm installation and maintenance, which require similar vessels and logistics support as oil & gas. SEACOR Marine explicitly targets offshore wind in its strategy (the company notes it serves offshore wind developers alongside oil E&P). Industry-wide, offshore wind projects worldwide are projected to create a ~10% increase in OSV demand, particularly for specialty vessels to handle turbine installation, cable laying, and crew transfer. 2024 saw an uptick in orders for new vessels that can service both wind and oil sectors, often equipped with hybrid power systems (e.g. battery-equipped PSVs) to meet stricter environmental requirements. Government support for renewables (in Europe, and nascent in the U.S.) means this segment could be a long-term growth driver. However, it’s still a smaller portion of revenue for most U.S. companies compared to oil & gas support. Over time, as energy transition progresses, those firms that diversify into wind and other marine renewable projects may enjoy additional growth and resilience.

Fleet Modernization and Technology: After a decade of oversupply and aging assets, the industry is now trending toward modernizing fleets with more efficient and capable vessels. Notably, 2024 saw the first significant newbuild orders for OSVs in about ten years. Every OSV ordered in this new cycle has been specified with battery-hybrid propulsion or other green technology, highlighting a focus on fuel efficiency and lower emissions. This technological leap is partly driven by charterers (oil companies) prioritizing ESG and by high fuel costs making efficiency a competitive advantage. Additionally, digitalization and automation are creeping in: about 12% of OSVs are now being equipped with advanced automation systems to enhance efficiency and cut operating costs. In subsea services, technology is also a driver – for example, Oceaneering and others are developing resident ROV systems and autonomous underwater vehicles, which could eventually allow more inspection work to be done remotely (reducing the need for large crews offshore). Companies investing in modern, versatile assets are better positioned to win contracts, as customers value reliability and performance. This trend favors larger, well-capitalized players (like Tidewater or TechnipFMC) that can afford new technology, and it raises the bar for any new entrants.

Consolidation and M&A Activity: Years of downturn forced industry consolidation, and that trend continued into the recovery as companies seek scale and efficiency. Larger fleets and broader service offerings enable better geographic coverage and cost-spreading. Tidewater’s acquisition of GulfMark in 2018 and more recently Swire Pacific Offshore in 2022 greatly expanded its fleet, making it the dominant OSV owner globally. In the international arena, 2023 saw Norway’s DOF Group acquire Maersk Supply Service, another sign of consolidation to remove competitors and rationalize vessel supply. Even smaller deals, like Edison Chouest Offshore (a U.S. private firm) acquiring ROV operator ROVOP, show service providers vertically integrating to offer turnkey solutions (in this case, pairing vessels with in-house robotics capability, possibly to serve offshore wind clients). The result of consolidation is an industry with fewer, stronger players – which can improve pricing discipline. For U.S. public companies, this means the competitive landscape is a bit less fragmented than in the past. Scale and consolidation are likely to continue as those with the means acquire distressed or smaller operators (e.g., one could envision Tidewater or others picking up assets from weaker rivals like SMHI if the opportunity arose). Overall, M&A is both a driver (expanding capabilities) and a response to industry trends (dealing with oversupply), and it has helped position the surviving companies for the current upturn.

Macro Demand for Energy & Hydrocarbon Supply Gaps: On a high level, rising global energy demand – projected to grow roughly 10% from 2020 to 2030 – underpins the need for new offshore oil and gas developments. Many oil companies are turning back to offshore projects (some of which have lower unit costs and larger reserves than short-cycle shale) to ensure supply in the late 2020s. Notably, after the Russia-Ukraine conflict in 2022, energy security concerns pushed countries and majors to reconsider offshore projects (e.g. gas developments in the Middle East and deepwater oil in Brazil) to diversify supply. This macro environment has been a tailwind for the offshore services industry: higher sustained oil prices and the imperative to replace declining onshore production make offshore attractive again. In addition, certain resource basins (Brazil’s pre-salt, Guyana’s recent discoveries, Gulf of Mexico deepwater) are extremely competitive barrels with break-evens viable even in a lower price scenario, so development is full-steam ahead. This broad-based demand for offshore resources translates to robust multi-year pipelines of work for service companies. Even though the energy transition is ongoing, most forecasts show oil and gas will remain significant through 2030, and offshore will play a key role – implying that the current upcycle for service providers could have legs for several years, barring a collapse in oil prices.

In summary, the offshore/marine services industry is benefiting from a confluence of positive trends: a cyclical upswing in oil & gas activity, secular growth from offshore renewables, and a pruning + modernization of capacity after the last downturn. Day rates and utilizations are up, and companies are investing in technology and scale. These drivers have improved the outlook for 2025 and beyond, though companies must also navigate challenges such as cost inflation, supply chain issues for new equipment, and the ever-present cyclicality of oil prices which can quickly change the equation.

🏆 Key Success Factors and Profitability Drivers

In an industry as challenging and capital-intensive as offshore services, operational excellence and strategic positioning are crucial to driving profitability. The following are key success factors that determine which companies thrive:

Modern, Efficient Fleet and Equipment: A company’s asset quality directly impacts its costs and the rates it can charge. Newer vessels and helicopters offer better fuel efficiency, higher reliability, and often enhanced capabilities (e.g. dynamic positioning, larger decks, hybrid power). This translates into lower operating costs and a premium in the market. Firms like Tidewater and SEACOR Marine that invested in more technologically advanced, green vessels are reaping benefits through fuel savings and customer preference for efficient tonnage. Similarly, TechnipFMC’s cutting-edge subsea equipment and Oceaneering’s latest ROV technologies can command strong margins due to their performance advantages. Maintaining a modern fleet also means higher utilization – clients tend to contract the most capable assets first, leaving older, less efficient units idle. Thus, success comes from continually upgrading the fleet and retiring or divesting obsolete assets to avoid a drag on earnings.

Scale and Utilization Management: Profitability in this sector heavily depends on keeping assets employed at remunerative day rates. Larger operators with global scale can more deftly achieve high utilization by moving assets to wherever demand is strongest and leveraging relationships with major customers in multiple regions. Tidewater’s global presence, for example, allows it to shift vessels between West Africa, the Middle East, or Latin America as opportunities arise, minimizing idle time. Scale also gives bargaining power with suppliers and the ability to spread fixed costs (like shorebase support and crewing logistics) over a wider revenue base. Smaller companies, in contrast, might have half their fleet stacked in a weak region while missing opportunities elsewhere. High utilization, combined with disciplined cost control, expands EBITDA margins considerably in the up-cycle. This factor showed clearly in 2024 results – Tidewater’s vessel utilization and scale efficiencies helped drive its EBITDA margin above 30%, much higher than peers with less scale (like SMHI) who struggled to cover fixed costs when a portion of their fleet was underutilized.

Contract Mix and Pricing Strategy: The structure of contracts and pricing strategy is a key determinant of profitability. Companies that locked in long-term contracts at or near cyclical lows might ensure stability but miss out on upside when the market tightens. Conversely, those with exposure to the spot market or short-term contracts can quickly benefit from rising rates (as seen with many OSV operators recently) but also face volatility. An optimal strategy can be a mix – for instance, secure long-term deals for a base level of utilization (covering costs) and leave some assets available for short-term high-rate work. Additionally, focusing on higher-margin niches is important: Helix, for example, pursues specialized well intervention contracts that carry premium rates versus generic vessel jobs, helping its margins (when execution is efficient). Contract execution and cost management also drive margin – delivering services on time and on budget yields better profitability and repeat business. Companies that consistently manage projects well (TechnipFMC in subsea installations, for instance) can avoid cost overruns and earn incentive fees, boosting their returns.

Geographic and Client Exposure: Not all offshore markets are equal – profitability can hinge on where a company operates and who its customers are. Certain regions like the U.S. Gulf of Mexico have historically had lower day rates and higher competition, pressuring margins, whereas markets like Brazil or the Middle East currently have such strong demand that vessel rates are much more lucrative. Companies with a footprint in the hot regions (Brazil deepwater, Qatar/Middle East gas, North Sea wind, etc.) have an edge. For example, TechnipFMC and Oceaneering benefit from Brazil’s aggressive development of pre-salt fields (a high-demand, high-spec work environment). Meanwhile, SEACOR Marine cited that its lackluster 2024 was partly due to slow activity in the U.S. Gulf and West Africa – illustrating the importance of region selection. Customer mix is also key: national oil companies and supermajors tend to demand high safety and reliability (favoring the best operators) but also have deep pockets for long campaigns, which can be lucrative if won. Having strong relationships and a track record with these big clients often leads to contract renewals and sole-source opportunities. By contrast, serving many small independent operators could mean more competitive bidding and credit risk. Therefore, cultivating a strong client base in the most active offshore basins drives more consistent and profitable business.

Operational Excellence: Safety and Personnel – The offshore environment is high-risk, so safety performance and skilled personnel are critical differentiators. Oil companies will favor service providers with exemplary safety records, since accidents offshore can be extremely costly and dangerous. A good safety track record not only helps win contracts but also avoids downtime and liability costs that directly affect profitability. Skilled crews and engineers are equally vital: experienced mariners, pilots, ROV operators, and subsea engineers perform tasks faster and more reliably, improving project economics. Companies that can attract and retain top talent thus have a competitive advantage. As Helix Energy Solutions notes, in this competitive contracting industry, beyond price, success depends on “the ability to acquire specialized vessels, attract and retain skilled personnel, and demonstrate a good safety record”. In recent years, a shortage of qualified vessel crews and pilots (after many left during the downturn) has made talent a limiting factor; firms that invest in training and maintain an engaged workforce can ensure they have the capacity to take on more work safely, thereby driving higher revenue and profitability.

Financial Discipline and Capital Allocation: Given the cyclicality, companies that manage their capital expenditure and balance sheets prudently tend to outperform over the cycle. Profitability in this context isn’t just about operating margin, but also returns on capital and cash flow. The last industry downturn revealed the dangers of over-leveraging and over-ordering assets – many companies went bankrupt as debt piled up and utilization crashed. Those that survived (or re-emerged) did so by restructuring debt and being very cautious with new investment. Now in the recovery, a key test is how disciplined management remains: avoiding a spree of speculative newbuilds and instead sweating existing assets can yield higher free cash flow which can pay down debt or be returned to shareholders. Tidewater’s strategy has been a good example – despite high demand, it has not rushed to build new vessels in U.S. shipyards (which would be costly), but is instead squeezing more out of its current fleet and selectively acquiring or reactivating idle vessels when economically justified. This has led to improving return on capital and cash generation for them. TechnipFMC, likewise, after its spin-off, focused on higher-margin integrated projects and kept R&D and capex targeted, which improved its overall returns. In short, profitability is enhanced when companies deploy capital wisely – timing new investments to demand, keeping leverage manageable, and opportunistically consolidating or exiting lines of business that don’t meet return thresholds.

By focusing on these success factors – modern assets, high utilization, smart contracting, advantageous market positioning, operational excellence, and financial discipline – the top companies manage to achieve superior margins and returns in an inherently challenging industry. The contrast in performance within the peer group often comes down to how well each company executes on these fronts.

💼 Porter’s Five Forces Analysis (Offshore/Marine Services)

Threat of New Entrants: Moderate. The offshore marine services sector has high barriers to entry in terms of capital requirements and industry know-how, but not so high as to completely lock out new players. To enter, a newcomer would need to acquire expensive offshore vessels or aircraft and skilled crews, plus establish safety credentials – a formidable undertaking. The market’s reliance on large, high-capital assets inherently makes it hard for small operators to break in. For example, a single modern deepwater PSV can cost tens of millions of dollars, and specialized intervention vessels are even pricier. New entrants also face regulatory and client trust barriers; oil companies are risk-averse and prefer contractors with proven track records (for safety and reliability). These factors favor incumbents. However, during boom times the door isn’t entirely closed – capital can be raised if optimism is high, and indeed historically we saw new entrants order vessels during upcycles (e.g. a number of new OSV companies emerged in the 2010-2014 boom, contributing to oversupply). There are also lower segments (shallow-water, small crew boats) that are easier to enter. Overall, while significant capital and experience are required (keeping the threat somewhat low), the cyclic nature means when day rates soar, shipyards will build for anyone with financing, making entry possible. Thus, the threat of new entrants is contained but not negligible: established players have an advantage, yet must be mindful that an overheated market can attract new competition.

Bargaining Power of Suppliers: Low to Moderate. Suppliers to this industry include shipbuilders, aircraft manufacturers, equipment providers (engines, ROV components), and labor (crew). Some of these suppliers are fairly concentrated, which can give them bargaining power. For instance, offshore helicopter operators rely on a few manufacturers (Airbus, Sikorsky, Leonardo) – a limited pool that can set high prices for new aircraft or parts. Vessel owners source from shipyards; while there are many global yards, those capable of high-spec OSVs are fewer (in the U.S., Jones Act-compliant builds are limited to domestic yards, which are costly). During downturns, however, shipyard demand dries up, and builders have little power – newbuild prices even fell as yards vied for scarce orders. Currently, with orders just beginning to resume, yards have some negotiating leverage but are not overloaded yet. Equipment and maintenance suppliers (for engines, DP systems, etc.) similarly have moderate power – they are specialized but there are alternate vendors in many cases. Labor is a critical “supplier”: skilled mariners, ROV pilots, and helicopter pilots. Lately, a shortage of experienced crew has given labor increasing leverage – wages have been rising, and companies sometimes have to pay premiums or bonuses to attract talent for tough offshore assignments. This erodes profit if not managed, indicating some power on the supplier (labor) side in a tight job market. However, overall, the supplier power is kept in check by the fact that marine service firms can switch or globalize their supply chain (e.g. purchase vessels second-hand if newbuild costs are too high, outsource maintenance to different vendors, etc.). In summary, suppliers have limited to moderate bargaining power. Key items like fuel are often a pass-through cost to clients, further reducing supplier influence on margins. Only in certain niches (say, a proprietary technology needed for a project, or a unionized labor group) does supplier power significantly bite.

Bargaining Power of Buyers (Customers): High. The buyers are predominantly large oil and gas companies (and to a smaller extent wind farm developers or government agencies). These customers are typically very powerful – they have deep technical knowledge, procurement teams that run competitive tenders, and often multiple service providers to choose from (especially in oversupplied markets). In the prolonged downturn (2015–2020), buyers exerted tremendous pressure on offshore service rates, driving them to unsustainable lows and forcing providers to accept slim margins or risk losing work. Because the oil majors and national oil companies control the project flow, they can dictate terms when capacity exceeds demand. For example, in the OSV segment, short contract tenures and spot hiring became common, giving E&P operators flexibility to switch providers frequently and keep prices down. Even in specialized areas, buyers can pit a few competitors against each other – e.g. for ROV services or well intervention, an operator might solicit bids from Helix, Oceaneering, and a couple of regional players, leveraging price as a key factor. The only mitigating factor is that in the current cycle, the market has tightened, shifting some leverage back to suppliers (service companies) in segments like high-end OSVs or certain subsea hardware – in other words, when there’s scarcity of a service (high utilization), the buyer’s power is blunted since they cannot easily find substitutes or spare capacity. But as a structural force, oil companies (the buyers) tend to have the upper hand: they are large, few in number relative to the service supply base, and their spending decisions can make or break service company performance. Therefore, buyer bargaining power is generally high. Service firms often have to accept onerous contract terms, and only differentiated technology or an exceptionally tight market allows them meaningful pricing power.

Threat of Substitutes: Moderate. Direct substitutes for the core services are limited – you need a vessel to move cargo offshore, or a helicopter to quickly transport crew to a distant platform. There is no simple technological substitute for a work-class ROV performing an underwater repair (aside from another ROV from a competitor). However, in a broader sense, there are a few substitutes or alternatives that can reduce dependence on these services. One is the option of onshore or alternative development: for oil companies, the “substitute” to hiring offshore services is to invest in onshore shale or other energy sources instead of offshore projects. Indeed, the shale boom last decade served as a substitute that diverted investment away from offshore – this indirectly reduced demand for offshore services dramatically. That dynamic can reoccur if onshore opportunities are more attractive. Within offshore operations, there are some substitution possibilities: for example, a drilling rig can sometimes be used to perform well maintenance that a well intervention vessel (like Helix’s) would otherwise do – in a soft rig market, an operator might contract a drilling rig to do plug & abandonment, substituting away from a specialized vessel. Another example: crew transfers could be done by boat instead of helicopter for installations closer to shore (trading speed for cost savings), so a marine crew vessel can substitute a portion of what Bristow’s helicopters would do, or vice versa. There are also emerging technological substitutes on the horizon: autonomous drones for deliveries, unmanned vessels, etc., though these remain experimental for now. Alternative energy and production methods can be seen as substitutes too – e.g. offshore wind is actually a new customer for marine services, but if the world aggressively shifts to renewables, it substitutes demand for offshore oil and gas (thus fewer rigs, vessels, etc., needed in long run). All told, while there is no one-for-one immediate substitute for most services (a platform still needs its supply vessel), the threat of substitution manifests in customers having different ways to achieve an outcome. Because oil companies can change development strategies (offshore vs onshore vs not developing at all) and can sometimes improvise (using different tools to do a job), the substitute threat is moderate. It is not as directly threatening as in some industries but remains a factor – particularly the competition from onshore oil and alternative energy investments which can reduce the addressable market for offshore services.

Competitive Rivalry: High. Rivalry among existing service providers in the offshore marine segment is intense. The industry has historically been fragmented and prone to overcapacity, leading to aggressive competition on price and terms. As noted, one of the long-standing challenges was that too many vessels were chasing too little work, especially after the 2014 oil crash, due to years of overbuilding. This led to cut-throat pricing – day rates fell below cash break-evens, and companies still kept vessels working just to cover some costs, indicating a highly rivalrous environment. Even as consolidation has occurred, we still see multiple players in each niche: for OSVs, aside from Tidewater and SEACOR, there are regional and private operators (Hornbeck, Edison Chouest, foreign players entering certain markets) that keep competitive pressure high. For helicopter services, Bristow faces competition from PHI and others in various locales. In subsea services, Oceaneering, Helix, TechnipFMC, plus Subsea7, Fugro, and others overlap in areas like inspection or light construction – all bidding for contracts. When demand slumps, rivalry spikes because everyone fights for a smaller pie, often resulting in price wars and bankruptcies (indeed, both Tidewater and the old Bristow went bankrupt in the last downturn, underscoring how brutal the competition became). Even in the current upturn, rivalry is present as companies jostle to position themselves for new opportunities. The recent improvement in market conditions has eased some price pressure, but also note that some new entrants (or reactivated competitors) are coming back, and the industry remembers the oversupply “dark cloud” that kept day rates weak for years. On non-price dimensions, competition revolves around service quality, safety, and capabilities – but ultimately contracts often come down to cost if multiple competent suppliers are available. The high fixed-cost nature of the business (vessels and helicopters are expensive whether or not they’re in use) means operators have a strong incentive to compete and win work even at low margin, rather than have assets idle. This dynamic fuels rivalry. Overall, the competitive rivalry is high in offshore/marine services, though it can oscillate between extremely high in downturns to somewhat tempered in boom times. The recent consolidation may reduce the number of bidders in some tenders, but as of early 2025 the industry is not yet a tight oligopoly – competition remains robust in all segments.

💵 Financial Metrics Analysis (Profitability & Efficiency)

To further differentiate the companies, we examine key financial and efficiency metrics – in particular, EBITDA margins, Return on Capital, and Free Cash Flow margins.

")

As shown in the EBITDA margin chart, profitability at the operating level collapsed during the 2015–2020 downturn – many companies saw EBITDA margins fall to zero or even negative in the worst years – and has since recovered dramatically. By the end of 2024, Tidewater stands out with an EBITDA margin of ~33%, the highest of the group. Tidewater’s margin leadership reflects the strong rebound in vessel day rates and utilization; as a predominantly OSV company, it benefits greatly from operating leverage (fixed costs spread over more revenue). Its margin was negative around 2018–2019 when many of its vessels were stacked, but as of 2024 it has expanded to roughly one-third of revenue, an impressive turnaround. Helix and TechnipFMC are in the second tier of EBITDA margins, around 20% and 16% respectively. Helix’s margins improved as it refocused on higher value-added well work and absorbed the Alliance acquisition (though Helix did experience margin dips in 2020–2021 when some vessels were underutilized). TechnipFMC’s mid-teens EBITDA margin is notable given its manufacturing component – it has managed to keep solid project execution and benefitted from cost cuts post spin-off, steadily improving from low-teens toward upper-teens. Bristow and Oceaneering are around the mid-teens (roughly 14–15% EBITDA margin), reflecting more stable, service-contract-oriented business; these two didn’t dip as severely into the negatives during the downturn, but also haven’t peaked as high as the pure OSV play. SEACOR Marine (SMHI) trails with the lowest EBITDA margin, about 10% – however, this is actually a positive swing from deeply negative EBITDA in 2018–2020 for SMHI. The chart indicates SMHI had the most severe margin trough (it appears to have hit –30% or worse EBITDA margin at the bottom), likely due to a very underutilized fleet and high operating overhead for its size. By 2024, SMHI clawed back to positive double digits, but it remains the least profitable at the EBITDA level among peers. Overall, industry EBITDA margins have improved across the board in the current upcycle, highlighting much healthier operations. The spread between Tidewater (top) and SMHI (bottom) underscores how scale and asset utilization drive superior operating leverage – with Tidewater now roughly twice as profitable (margin-wise) as several peers. The cyclical nature is clear too: all lines trend upward into 2023–2025 after the nadir around 2018–2020, showing the effect of the rising tide of offshore activity lifting all boats’ operating performance.

")

The chart above illustrates that for much of the last decade, ROIC was abysmally low – often negative – for offshore service companies, due to oversupply and weak earnings. Coming into the current upturn, we finally see ROCs turning positive and improving. As of LTM 2024, TechnipFMC (FTI) leads with about a 14% Return on Capital, the highest among the peers. FTI’s relatively asset-light approach (it provides a lot of engineering and subsea kit, and although it has vessels, it partners for many installation scopes) and strong project margins on recent contract wins have yielded a solid ROIC. It also shed some capital-intensive businesses during its restructuring, which improved capital efficiency. Oceaneering (OII) and Tidewater (TDW) follow with roughly 10–11% ROC. For Tidewater, hitting ~10% ROIC is a notable achievement given that for years post-bankruptcy its returns were negative – this reflects how dramatically vessel utilization and pricing gains have boosted its earnings relative to its fixed asset base. Oceaneering’s ~11% indicates decent profitability on its deployed capital; its mix of services and products, and a portion of government contracts, give it fairly stable earnings against a base of ROVs and equipment that are now better utilized than a few years ago. Bristow (VTOL) is around 5% ROC, and Helix (HLX) around 4% – these low single-digit returns suggest that, despite the recovery, those two are still not earning robust returns above their cost of capital. Bristow’s business (aviation services) traditionally has lower ROIC due to the high cost of helicopters and moderate margins on long-term contracts; its current ROIC in mid-single digits is likely below what investors would consider a good return, although it’s an improvement from negative returns during its restructuring in 2019. Helix’s 3–4% ROIC indicates it is just barely profitable relative to its asset base – the company had negative returns in the downturn, and even now, with some vessels still ramping up work and certain contracts at lower rates, its returns are subpar. Finally, SEACOR Marine (SMHI) unfortunately still shows a negative Return on Capital (~–2% LTM). This means SMHI’s net operating profit is still slightly in the red relative to the capital deployed; effectively, it is destroying value at the moment (likely due to interest and depreciation outpacing operating income). SMHI had deeply negative ROIC in 2018–2020 (as the chart suggests, possibly –8% or worse at the trough), and while it has improved, it has not yet crossed into positive territory, reflecting ongoing losses or very low operating income. The trend overall is that ROCs are rising after bottoming out around 2018–2020 – a very important development for the industry’s health. But only a couple of companies (FTI, OII, TDW) are currently achieving double-digit returns, which is roughly the minimum threshold for covering cost of capital in this industry. The data underscores that while the cycle is improving profitability, some firms still have work to do to justify the heavy investment in their assets. Leaders like TechnipFMC are demonstrating they can earn solid returns via differentiation and volume, whereas laggards like SMHI are still in turnaround mode.

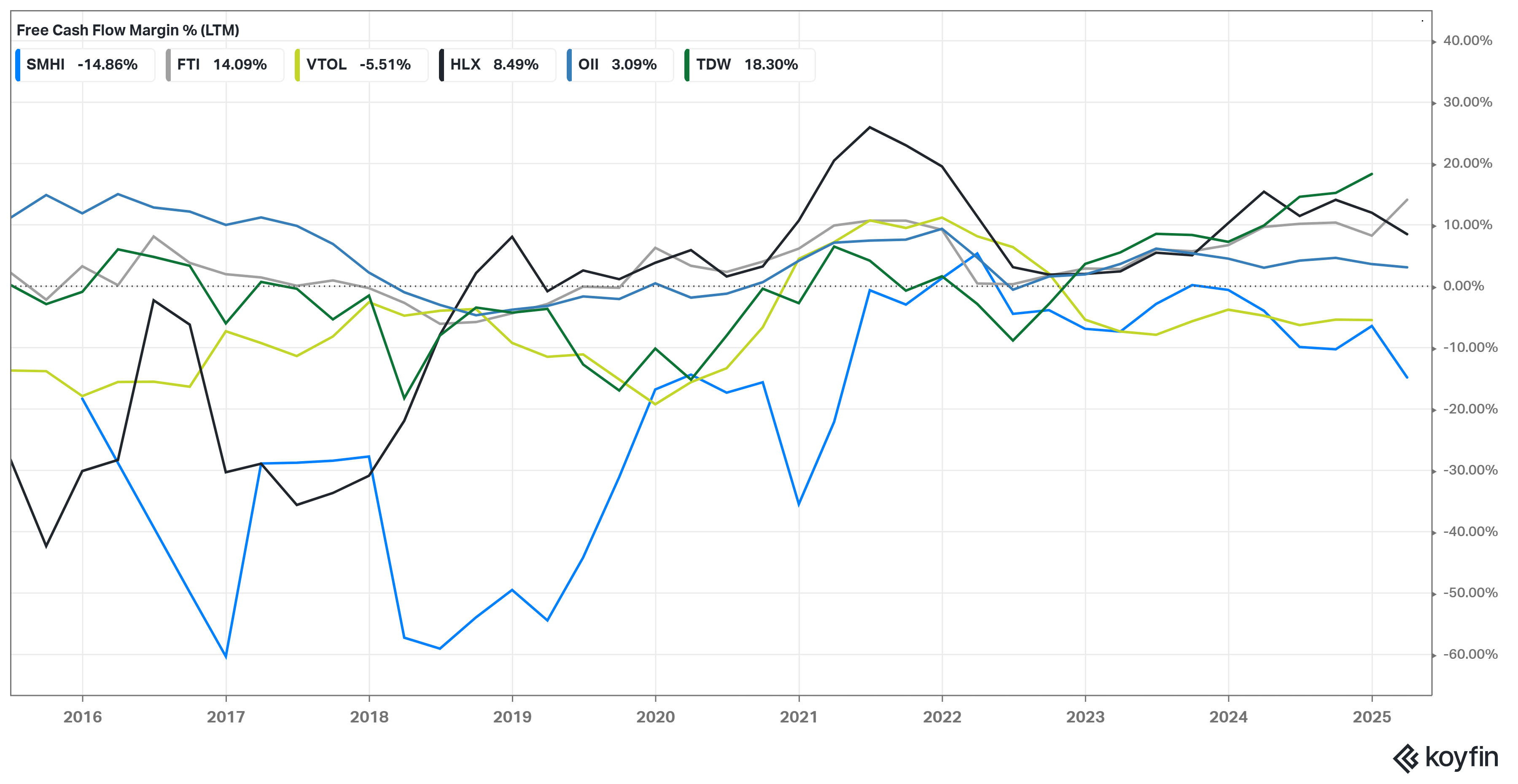

The chart shows that during the downturn years, most companies had negative free cash flow margins – not surprising, as revenues were low and many still had maintenance capital expenditures to keep fleets operational, resulting in cash burn. By 2022–2024, however, there has been a marked improvement. Tidewater (TDW) now boasts the highest FCF margin at around 18%, meaning it retains a substantial portion of revenue as free cash. In 2024, Tidewater generated $331 million of free cash flow (almost 200% higher than the prior year), thanks to strong operating cash flow and relatively restrained capex. This reflects both the robust EBITDA and the fact that Tidewater, having a modern fleet post-bankruptcy and acquisitions, did not need to spend heavily on new vessel construction – so a good chunk of its earnings translate to free cash. TechnipFMC (FTI) also shows a healthy FCF margin (~14%). In Q4 2023 alone, TechnipFMC reported $630 million in free cash flow (due in part to milestone payments), illustrating its ability to turn profits into cash, aided by its asset-light service components and careful project cash management. Helix (HLX) is in positive territory with ~8–9% FCF margin, which is a positive sign that Helix is generating cash (it likely curtailed growth capex and focused on integrating past investments). Oceaneering (OII) has only a modest FCF margin (~3%), basically around break-even free cash after necessary capital spending. Oceaneering tends to invest continuously in its ROV fleet and new technologies, so while it’s profitable, a lot of its operating cash gets reinvested, leaving only a small free cash yield. The concerning ones are Bristow (VTOL) and SEACOR Marine (SMHI), which both still show negative FCF margins (approx –5% for VTOL and –15% for SMHI). Bristow’s slight negative free cash flow suggests that even though it’s operationally profitable, its capital expenditures (perhaps on fleet maintenance, new helicopter purchases, or lease payments) outweighed operating cash in the last LTM period. SMHI’s –15% FCF margin is more worrying: it indicates significant cash burn. SEACOR Marine had to invest in reactivating vessels and placing orders for new hybrids, and its operating cash flow was not sufficient to cover that, hence a large negative free cash outcome. Historically, SMHI had some years of extremely negative FCF (the blue line dives deeply around 2017, possibly –50% or worse, when it spun off and had to invest in its fleet), then a period of improvement (even briefly positive in 2021 when they may have sold assets or cut capex), and then back to negative as of 2024.

The volatility of the free cash flow lines in the chart underscores how capital-intensive and cyclical the sector is – companies swing from burning cash in bad times to generating surplus in good times, depending on how they manage capex. The current snapshot shows Tidewater and TechnipFMC as clear leaders in cash generation, which aligns with their strong margins and disciplined investment. Helix and Oceaneering are doing alright, maintaining positive if not huge FCF. Meanwhile, Bristow and SMHI need to achieve better cash flows – either by improving operating profits or by scaling back capex – to strengthen their financial position. Investors typically favor those companies that can generate free cash consistently, as it indicates the business is self-funding and potentially able to return capital. In that sense, Tidewater’s nearly $0.20 of every $1 in revenue becoming free cash is a very attractive metric, signifying the turnaround of its fortunes and prudent capital management in the upcycle.

💡 Investment Conclusion

Based on the foregoing analysis of market dynamics, financial performance, and strategic positioning, the most attractive investment opportunities in the U.S.-domiciled offshore/marine services industry appear to be Tidewater Inc. (TDW) and TechnipFMC (FTI). These two companies distinguish themselves with strong growth trajectories, improving profitability, and solid strategic footing in the recovering offshore market:

Tidewater (TDW) – Tidewater offers a compelling pure-play exposure to the offshore oil & gas rebound. It has emerged as the market leader in offshore vessel services, and is translating that leadership into exceptional financial results. Tidewater is growing revenue faster than any peer (33% YoY in 2024), and more importantly, it is converting the upturn into high margins and cash flow. Its EBITDA margin (~33%) and FCF margin (~18%) are the best in class, reflecting both the strong demand environment and Tidewater’s internal efficiency (post-bankruptcy, its cost base is lean and fleet composition optimized). The company’s global scale and fleet size allow it to serve the most active drilling markets (West Africa, Middle East, Brazil) and command top-tier day rates, which should sustain revenue growth into 2025 (albeit at a somewhat moderated pace as the easy gains have been realized). Crucially, Tidewater has also shown capital discipline – rather than rushing to build new vessels at high cost, it has focused on reactivating and modestly upgrading its existing fleet, and even returned cash to shareholders (buying back $90 million in shares in 2024). This strategy means high free cash flow can continue, enabling debt reduction or further buybacks. With offshore upstream spending set to remain robust through mid-decade, Tidewater is positioned to harvest strong profits from a tight OSV market. Its recent net income of $180.7M in 2024 (86% higher than 2023) demonstrates a sharp earnings inflection. From an investment standpoint, Tidewater provides leverage to the cycle with comparatively lower risk now (its balance sheet is healthy, and industry oversupply has diminished through scrapping and consolidation). The primary risk would be a downturn in oil prices reducing rig activity, but absent that, Tidewater stands to benefit from the multi-year offshore upcycle and therefore looks very attractive.

TechnipFMC (FTI) – TechnipFMC represents a more diversified and technologically differentiated opportunity. Unlike Tidewater’s focus on day-rate shipping, FTI is a leading subsea systems and services provider with a global franchise. The investment thesis for FTI is underpinned by its record-breaking backlog and order intake, which give high revenue visibility for the next several years. FTI’s subsea orders grew 45% in 2023 to $9.7B, boosting backlog to $13.2B – a clear signal that oil companies are sanctioning many new offshore projects and entrusting TechnipFMC with those developments. This backlog will translate into rising revenues and, with execution, solid earnings. Already FTI’s financials are improving: it delivered ~22% YoY revenue growth in Q4 2023 and is generating substantial free cash flow (over $600M in a quarter as noted). The company’s return on capital (~14%) is the highest of the peer group, indicating it is utilizing its assets and intellectual property effectively. Strategically, TechnipFMC has an edge due to its integrated project model (iEPCI) and leading technology in subsea hardware – this differentiation protects its margins and gives it a quasi-“moat” in a segment where not many can compete at its scale. As offshore developments grow in complexity (e.g. deeper water, tie-backs, subsea processing), FTI is often the partner of choice, which should ensure it remains booked and can negotiate favorable contract terms. From an investor perspective, TechnipFMC offers a balance of growth and stability: its backlog acts somewhat like a cushion (reducing downside risk of revenue shortfall), and its growing services segment provides recurring income. The company reinstated shareholder payouts (buybacks/dividends ~$249M in 2023), which is a positive sign of confidence in its cash flows. Additionally, FTI has exposure to the energy transition through offerings in areas like floating wind and carbon transport (though small today, it could add optionality long-term). Overall, FTI is attractive as a pick-and-shovel play on offshore development – as more fields get built under the sea, FTI’s earnings and cash should swell.

Both Tidewater and TechnipFMC thus stand out – Tidewater for cyclical torque and cash generation, and TechnipFMC for order-driven growth and tech leadership. If one were constructing a portfolio, these two complement each other (one is more asset-heavy, one more tech/service-oriented; one tied to short-term spot rates, one locked-in longer term).

Among the others, Oceaneering (OII) and Helix (HLX) have merits but are slightly less compelling at this point. Oceaneering is a solid company with diverse capabilities and improved returns (ROC ~11%). It should benefit from both oil and wind projects (and its defense segment provides some stability). Its upside may be more limited, though, as it already operates at decent capacity – OII feels like a steady performer rather than a breakout growth story. Helix has a unique niche in well intervention and decommissioning, which could see greater demand as offshore fields age and as operators seek cost-efficient ways to boost production. However, Helix’s recent execution has been mixed (flat revenues, low ROIC), and it carries some risk if it cannot secure enough utilization for its vessels outside core contracts. Helix could be a turnaround/value play if one believes the need for well interventions will spike (for example, if high oil prices push operators to work over many existing wells), but it’s a bit speculative until its financial metrics improve.

Bristow (VTOL) and SEACOR Marine (SMHI) appear less attractive near-term. Bristow does provide a relatively stable business (it has long-term contracts and even government SAR revenue that is insulated from oil price swings), but that stability comes with low growth and currently negative free cash flow. Its upside from the offshore recovery is more limited compared to vessel operators, and it faces unique risks (like operational hazards of aviation and potential contract rebids for SAR). SEACOR Marine, meanwhile, is still trying to regain footing – it has high leverage to the OSV cycle like Tidewater, but its results lag far behind. Given SMHI’s persistent losses and cash burn, an investor might wait to see evidence of a sustained turnaround (e.g. successful deployment of those new hybrid vessels and a return to positive EBITDA growth) before jumping in. It’s also relatively thinly traded and smaller cap, which may not suit all investors. Essentially, Bristow and SMHI rank lowest on the investment appeal due to their financial underperformance and in SMHI’s case, a riskier balance sheet.

In conclusion, Tidewater and TechnipFMC emerge as the top picks in the U.S. offshore services space as of early 2025. Tidewater offers exposure to the increasing volume and pricing in offshore logistics with outstanding current financial performance, while TechnipFMC provides a growth story backed by record backlog and a differentiated market position in subsea technology. Both companies are benefiting from favorable industry trends and have demonstrated improving efficiency (high margins/ROIC) which should translate to continued shareholder value creation. An investor bullish on offshore oil & gas recovery would likely overweight Tidewater for maximum cyclicality, whereas an investor looking for a slightly more diversified and longer-term growth play might favor TechnipFMC – but a combination of the two could capture both dimensions. With offshore drilling activity expected to remain strong (even if growth moderates) and energy companies continuing to invest in new projects, these companies are well positioned to outperform their peers. As always, one should monitor oil price trends and capital discipline (to avoid the mistakes of past booms), but as of now, TDW and FTI seem to offer the best risk-reward in the industry, supported by both their financial metrics and strategic outlook.