Bayer A.G. (BAYZF), Corteva, Inc. (CTVA), Nufarm Limited (NUFMF), FMC Corporation (FMC), American Vanguard Corporation (AVD), Bioceres Crop Solutions Corp. (BIOX), Bayer Aktiengesellschaft (BAYRY), BASF SE (BASFY)

Crop protection is the branch of agriculture focused on products that safeguard crops from pests, weeds, and diseases. This includes chemical pesticides (herbicides for weeds, insecticides for insect pests, fungicides for diseases) as well as emerging biological alternatives. These inputs are critical for global food production – without effective crop protection, farmers could lose nearly half of their crop yields to pests and diseases. By preventing such losses, crop protection products help ensure food security, improve farm productivity, and optimize land use.

🏭 Key Companies

Corteva, Inc. (CTVA)

Market Position: Corteva is a leading pure-play agriculture company formed in 2019 via the spin-off from DowDuPont. It boasts a balanced portfolio of seeds and crop protection products, making it one of the global leaders in both segments. In crop protection, Corteva offers a full range of herbicides, insecticides, and fungicides (with flagship chemistries like Rynaxypyr insecticide and the new Enlist™ herbicide system for 2,4-D tolerance). The company has a global footprint, serving row-crop farmers in the Americas, Europe, and Asia, as well as specialty crop markets. Corteva’s customer base ranges from large commercial farms (where its integrated seed-chemistry solutions drive sales) to smaller growers via distributors. Its positioning emphasizes innovation and proprietary products – leveraging both its Dow/DuPont legacy actives and new molecules from in-house R&D – as well as integrated offerings (e.g. selling seeds bundled with compatible herbicides).

Recent Strategic Moves: Corteva has aggressively expanded into biological crop protection to complement its traditional chemistry portfolio. In late 2022 it announced acquisitions of Symborg (a microbial crop input company) and Stoller Group, one of the largest independent biologicals firms. These deals (worth ~$1.6 billion combined) closed in 2023, marking a major push into bio-based fertilizers, biostimulants, and biopesticides. They reinforce Corteva’s strategy to offer farmers more sustainable options and tap a high-growth segment. On the chemical side, Corteva has continued to launch new active ingredients (e.g. Arylex™ herbicide family) and trait-linked products (the Enlist™ weed control system tied to its herbicide-tolerant seeds). It has also exited older chemistries with regulatory issues (notably phasing out chlorpyrifos insecticide). Geographically, Corteva has expanded its reach in high-growth regions (e.g. increasing presence in Latin America and Asia) and maintained strong North American and European operations. Overall, Corteva’s strategy centers on innovation and a broad solution offering, from patented chemicals to seeds and emerging biologicals.

Nufarm Limited (NUFMF)

Market Position: Nufarm is an Australia-based mid-tier crop protection company historically known for its portfolio of off-patent (generic) agrochemicals. It produces herbicides (like glyphosate, phenoxy herbicides), insecticides, and fungicides, often focusing on post-patent active ingredients and niche products. Nufarm has a significant presence in Australia/New Zealand and Europe, with growing operations in North America and Asia. The company repositioned in recent years to focus on core crops in key regions after exiting less profitable markets. Notably, in 2020 Nufarm sold its entire South American crop protection businesses to Sumitomo Chemical for $800 million. This sale provided cash to deleverage and refocused Nufarm on regions with historically higher margins and more predictable performance (Australia, North America, and Europe). Nufarm’s customer base ranges from broadacre grain farmers to specialty crop growers, often served via distribution partners. It also has a seeds subsidiary (Nuseed), which is separate from crop protection but has developed innovative products like omega-3 canola and carinata – illustrating Nufarm’s broader ag solutions approach.

Recent Strategic Moves: After the Latin America divestiture, Nufarm has been streamlining and investing to improve profitability. The company brought in a strategic partner (Sumitomo had also taken a minority equity stake, though it was later divested) and undertook cost reductions and manufacturing footprint optimization. Nufarm’s strategy now emphasizes margin expansion over pure revenue growth – targeting an EBITDA margin of 20–25% by FY2026 (versus single digits in recent years) through efficiency and product mix improvements. On the product front, Nufarm continues to supply a wide range of generic crop protection chemicals, but is also investing in differentiated formulations and partnerships. For example, it leverages its proprietary “Nuseed” innovations by commercializing omega-3 canola oil for aquaculture feed (a departure from traditional pesticides), and is exploring bio-herbicides and new formulations in collaboration with research partners. The company has also strengthened its presence in Europe and North America, filling portfolio gaps with in-licensed products.

American Vanguard Corporation (AVD)

Market Position: American Vanguard (through its main operating subsidiary AMVAC) is a specialty crop protection company based in the U.S. It has a niche portfolio of products, including soil and granular insecticides (e.g. Aztec® and Counter® for corn soil pest control), herbicides, and fungicides often used in high-value or specialty crops. AVD’s scale is much smaller than the global majors – annual sales are around ~$500–600 million – and it often targets specific market niches or geographies. The company serves both row-crop farmers (particularly in the U.S. for corn, cotton, etc.) and specialty crop markets (fruits, vegetables, turf/ornamental) via its diverse product line. A notable aspect of AVD’s positioning is its focus on “proven chemistries” (older off-patent actives) which it keeps in the market, and its development of application technology to differentiate itself. For instance, AVD introduced SIMPAS (Smart Integrated Multi-Product Prescription Application System) – a precision application technology that allows farmers to apply multiple products (insecticides, micronutrients, etc.) simultaneously at planting with variable rates. This foray into precision ag gear is unique for a company of its size and reflects an attempt to add value beyond the active ingredient.

Recent Strategic Moves: American Vanguard has been undergoing a business transformation initiative to improve efficiency and reignite growth. In 2023–2024, management launched cost-reduction and operational improvement programs aimed at eventually achieving ~15% EBITDA margins across the cycle (up from mid-single-digit levels recently). The company is also adjusting its portfolio: it completed small acquisitions such as AgNova in Australia (2020) and Punto Verde in 2023 to expand its presence and product offerings in certain markets (Australia and soil health, respectively). Simultaneously, AVD exited or is phasing out some older or problematic products – for example, it undertook a product recall of the herbicide Dacthal in 2024 due to regulatory issues, incurring one-time costs but reducing future liabilities. Strategically, AVD is investing in Green Solutions™ (bio-based and organic products) which saw revenue growth of 18% YoY in 2024, indicating a pivot to sustainable offerings. It also continues to emphasize its precision application technology and has a dedicated business for non-crop products (via AMGUARD for public health pest control). However, competition from generic producers remains a headwind – AVD noted pressure from generic alternatives as a factor impacting sales of key products.

FMC Corporation (FMC)

Market Position: FMC is a leading U.S.-based crop protection company, known as a pure-play agrochemical innovator. Over the past decade, FMC has vaulted into the top tier of global crop protection firms – it now generates roughly $5–6 billion in annual crop protection sales, putting it among the largest five companies globally. FMC’s product portfolio is weighted toward insecticides and herbicides, including several blockbuster proprietary products (for instance, the diamide-class insecticides acquired from DuPont and new herbicide chemistries in development). The company operates worldwide, with strong market share in the Americas and Asia, and a growing footprint in Europe. FMC distinguishes itself by focusing exclusively on crop protection (it has no seeds business) and by maintaining a pipeline of innovative active ingredients. It primarily serves growers of major row crops like soybeans, corn, rice, cotton, etc., via distribution networks. FMC’s customer strategy emphasizes technical expertise and value-added services (e.g. decision support tools through its Arc™ farm intelligence platform), which help position it as a solutions provider, not just a chemical seller.

Recent Strategic Moves: FMC’s trajectory in recent years has been marked by portfolio refinement and R&D breakthroughs. A pivotal move was its 2017 acquisition of a portion of DuPont’s crop protection portfolio (including the marquee Rynaxypyr™ and Cyazypyr™ insecticides and some herbicides), which transformed FMC’s scale and product mix. In exchange, FMC divested its legacy Lithium business, cementing its identity as a pure agriculture company. More recently, FMC has divested non-core units to focus on crop chemicals: in 2023 it agreed to sell its Global Specialty Solutions business (non-crop pest control segment) to Envu for $350 million, further streamlining around core ag markets. On the innovation front, FMC made headlines for developing the first new herbicide mode of action in over 30 years – the active ingredient tetflupyrolimet (branded as Dodhylex™), which controls resistant grasses in rice. This molecule (to be marketed as “Keenali™” herbicide) gained its first registration in 2023 and highlights FMC’s R&D capabilities. The company is also investing heavily in biologicals and precision ag through partnerships and research. For instance, FMC has multi-year collaborations with biotech firms on RNA interference (RNAi)-based insecticides and has partnered with Micropep and others to explore novel biocontrol solutions. In Brazil, FMC partnered with a local firm (Ballagro) to expand its biological portfolio. Additionally, FMC continues to build digital agriculture tools – its Arc™ farm intelligence platform uses AI to help farmers predict pest outbreaks and optimize pesticide use. Geographically, FMC has expanded manufacturing and formulation capacity in Asia (while navigating supply chain challenges for key ingredients). Collectively, these moves show FMC doubling down on innovation and high-value products (new modes of action, biologicals) while exiting lower-margin or non-ag segments. The strategy aims to keep FMC’s product lineup differentiated and its margins high in the face of rising generic competition.

Bioceres Crop Solutions Corp. (BIOX)

Market Position: Bioceres is a newer entrant, a Argentina-based agricultural technology company specializing in sustainable crop inputs. Much smaller in scale than the others (annual revenues ~$300–400 million), Bioceres focuses on biological crop protection and biotech traits. Its product portfolio includes microbial seed treatments, inoculants (through its subsidiary Rizobacter), bio-fungicides/insecticides, and crop nutrition products – positioning it as a leader in the agricultural biologicals niche. Bioceres is also known for its proprietary biotech trait, HB4® drought-tolerant technology, engineered in crops like soybeans and wheat. This trait, combined with compatible seed treatments, exemplifies Bioceres’ integrated approach to improving crop resilience. The company’s core market has been Latin America (especially Argentina and Brazil), but it has been expanding into North America, Europe, and other regions through partnerships and acquisitions. Customers include progressive farmers and ag retailers looking for eco-friendly solutions to boost yields and soil health. Bioceres often collaborates with larger firms for distribution; for example, it has worked with Syngenta to potentially commercialize HB4 wheat in new markets.

Recent Strategic Moves: Bioceres has pursued an aggressive growth-by-acquisition and innovation strategy to scale up. A landmark move was its merger with Marrone Bio Innovations (MBI) in 2022, a deal that combined two leading biologics portfolios. This merger created what Bioceres called a “global leader in sustainable agricultural solutions,” significantly expanding its bio-pesticide offerings and giving it a foothold in the North American market. Alongside MBI’s biopesticides, Bioceres also integrated MBI’s R&D capabilities in botanicals and pheromones. This came after Bioceres had already gone public via a SPAC in 2019, providing capital for expansion. The company continues to invest heavily in R&D for both biologics and biotech traits – aiming to achieve a ~22% EBITDA margin longer-term by focusing on proprietary, high-value products. On the biotech side, Bioceres achieved regulatory approvals for its HB4 drought-tolerant wheat in Argentina and Brazil, and is pursuing approvals elsewhere, which could open new revenue streams through seed and trait licensing. In sustainability initiatives, Bioceres launched the HB4 Program, a platform tracking carbon footprint and soil benefits of its technologies, to monetize environmental services. It also secured partnerships to distribute bio-solutions globally (e.g. with Syngenta for certain inoculants). Overall, Bioceres is growth-focused, leveraging M&A (the MBI merger, earlier acquisition of Rizobacter, etc.) and its unique biotech assets to rapidly increase scale. Its strategy targets the convergence of biotech traits, biologics, and digital agronomy to meet climate resilience and sustainability needs – positioning Bioceres at the forefront of the bio-based crop protection trend, albeit with the risks of a small, still unprofitable high-growth company.

Bayer AG – Crop Science Division (BAYRY)

Market Position: Bayer’s Crop Science division (formed after Bayer’s 2018 acquisition of Monsanto) is one of the world’s largest agricultural input businesses, encompassing both crop protection and seeds/traits. Focusing on crop protection, Bayer inherited a vast portfolio of herbicides (notably glyphosate via Monsanto’s Roundup brand, and glufosinate via the LibertyLink line), insecticides, fungicides, and digital farming tools. Bayer’s crop protection products include blockbusters like the fungicide Proline (prothioconazole), newer chemistries like foxastrobin, and legacy products now off-patent. It operates globally, with a top-two market share in all major regions, and serves virtually all crop sectors from corn, soybean, wheat, and rice to horticulture. Glyphosate-based herbicides remain a significant (if lower-margin) portion of Bayer’s crop protection sales, given Roundup’s ubiquity. Bayer’s customer strategy often integrates crop protection with its seed and trait offerings – for example, its Roundup Ready traits promote herbicide sales, and its Climate FieldView digital platform (acquired via Monsanto) helps farmers manage both seed and chemical decisions. In terms of innovation scale, Bayer (post-Monsanto) has the industry’s largest R&D budget, supporting discovery of new modes of action and next-generation traits.

Recent Strategic Moves: The past few years have been a period of integration and challenge for Bayer Crop Science. The $63 billion Monsanto acquisition (2018) vaulted Bayer into a leadership position but brought significant baggage, notably the Roundup (glyphosate) litigation. Bayer has been embroiled in lawsuits alleging Roundup’s health risks, and has allocated ~$16 billion for settlements and mitigation. This has forced strategic focus on containing legal liabilities and finding alternatives to glyphosate. Indeed, Bayer announced investments in developing new herbicide modes of action to eventually replace or complement glyphosate by the late 2020s, and it cut the price of Roundup as it became off-patent, seeking to maintain volume but accepting slimmer margins. In terms of portfolio, Bayer had to divest certain businesses to gain regulatory approval for Monsanto – it sold its LibertyLink herbicide and certain seed businesses to BASF in 2018. Post-merger, Bayer has concentrated on leveraging its trait-seed-chemical stack (e.g. Xtend cropping system combining dicamba herbicide with dicamba-tolerant soybeans) and expanding its digital agriculture services. Climate FieldView, Bayer’s digital farming platform, has been scaled up to millions of subscribed acres, providing farmers data insights on seed performance and chemical application, and bolstering customer stickiness. On the innovation front, Bayer Crop Science is pushing into biologicals and cutting-edge technologies: it partnered with Ginkgo Bioworks (Joyn Bio) to develop nitrogen-fixing microbes and with other startups on areas like RNAi biopesticides. It has publicly committed that by 2030, it will reduce the environmental impact of its crop protection portfolio by 30% (through safer chemistries and precision application), driving R&D toward lower-toxicity solutions. Regionally, Bayer has had to navigate stringent EU regulations – it has seen some active ingredients banned or non-renewed in Europe (like certain neonicotinoid insecticides), which has prompted a shift in R&D focus to other markets or new actives. Organizationally, Bayer’s new CEO (appointed 2023) is reviewing the company’s structure, leading to speculation of a potential future spin-off or IPO of the Crop Science division to unlock value. For now, Bayer Crop Science is a giant that is streamlining and innovating under pressure – managing legacy issues (glyphosate litigation, integration synergies shortfall) while continuing to launch new products (e.g. SmartStax PRO corn with RNAi trait, new fungicides like iblon) and champion digital & biological solutions for long-term growth.

BASF SE – Agricultural Solutions segment (BASFY)

Market Position: BASF’s Agricultural Solutions division is a top-four global crop protection business, housed within the larger BASF chemical conglomerate. It produces a wide array of crop protection chemicals – herbicides, fungicides, insecticides, seed treatments – and since 2018 has also had a seeds and traits portfolio. BASF’s ag chem portfolio is known for leading products like the Clearfield™ herbicide system (imazamox herbicide + tolerant crops), Liberty® herbicide (glufosinate), F500/Strobilurin class fungicides (pyraclostrobin), and more recently the novel Revysol® fungicide (mefentrifluconazole). The 2018 acquisition of assets from Bayer significantly expanded BASF’s presence: BASF gained the LibertyLink trait and glufosinate business, Bayer’s vegetable seeds, and certain field crop seeds (e.g. canola and soybean lines). This transformed BASF into a more full-spectrum ag player, though crop protection chemicals still account for the majority of its ~$9–10 billion ag segment sales. Geographically, BASF Ag Solutions has a balanced reach – strong in Europe (its home market), North America, and growing in Asia and Latin America. As part of a diversified company, BASF’s approach to customers emphasizes not just product sales but also agronomic services and digital farming tools (such as its xarvio® digital platform) to optimize chemical usage. The segment serves large-scale growers via channel partners and has some direct relationships through its digital offerings.

Recent Strategic Moves: BASF’s ag strategy has been driven by portfolio enhancement and innovation, tempered by the regulatory environment. The 2018 acquisition of Bayer’s divested assets (for ~€7.6 billion) was a major strategic move, instantly adding a profitable glufosinate herbicide franchise and seed capabilities. Since then, BASF has worked on integrating those businesses (e.g. launching LibertyLink traits in BASF’s own seed offerings) and realizing synergies. On the innovation side, BASF has introduced new active ingredients at a steady pace: notably the fungicide Revysol (launched ~2019) and a pipeline of herbicides in development (including at least one new mode of action herbicide expected later this decade). It is also expanding in biologicals – BASF had earlier acquisitions like Becker Underwood (2012) for biological seed treatments, and continues to partner on biopesticides and biostimulants. For example, BASF’s “GreenReach” program includes biofungicides like Serifel® (a Bacillus-based product). In digital farming, BASF’s xarvio Field Manager app provides farmers with zone-specific crop management recommendations and has seen increasing adoption, underscoring BASF’s commitment to data-driven agriculture. A key external factor is Europe’s tightening regulation: BASF has openly stated that the EU’s stricter approval process is forcing it to shift R&D investment toward other regions. In 2022, BASF announced it would wind down some European R&D and production in crop chemicals and focus on North America and APAC for growth, given the EU’s proposal to cut pesticide use significantly. Financially, BASF Agricultural Solutions has been a solid contributor to the parent company, with EBITDA margins around the high-teens to 20% range in recent years. There has been investor pressure for BASF to consider carving out or listing this division, which could unlock value since pure-play ag companies often get higher valuations. BASF so far keeps Ag Solutions as a core division, but it is managed for profitable growth with an emphasis on innovation (a pipeline targeting €7.5 billion in peak sales by 2034), portfolio balance (chemical & seed), and adaptation to sustainability demands (BASF offers a Carbon Farming initiative and is reformulating products to reduce environmental impact).

🤼 Competitor Strategy Comparison – Current Tactics and Differences

The crop protection players above employ differing strategies and tactics based on their strengths:

Product Focus and Innovation: Corteva, FMC, Bayer, and BASF all invest heavily in R&D to discover new active ingredients (AIs) and differentiated technologies. For instance, FMC and Bayer are racing to introduce new herbicide modes-of-action to combat resistant weeds, while Corteva and BASF also have robust pipelines. In contrast, Nufarm and American Vanguard rely more on off-patent chemistries and incremental innovation (formulations, mixtures) rather than discovering novel AIs. Bioceres pursues innovation in biologicals and biotech traits, carving a niche in sustainable tech rather than competing head-on in synthetic chemistry.

Integrated Solutions vs. Pure-Play: Bayer and Corteva are fully integrated – selling seeds/traits, crop chemicals, and digital services as a bundle. This allows cross-selling (e.g. trait seeds driving herbicide sales) and a broader value proposition to farmers. BASF is moving in that direction since acquiring seeds, though it remains primarily a chemical company. FMC, Nufarm, AVD, and Bioceres are pure-plays (or near-pure) in crop inputs without major seed businesses. They focus on chemical and biological product innovation and partner with seed firms when needed (e.g. FMC collaborates with Syngenta on certain tech, Bioceres licenses its HB4 trait to others). The integrated players often target enterprise-level solutions, whereas pure-plays tout agility and specialization.

Global Reach vs. Regional Focus: Bayer, BASF, Corteva, and FMC are truly global, with significant sales in all major ag markets (North & South America, Europe, Asia-Pacific). They can buffer regional shocks (droughts, currency swings) with diversification. Nufarm is intermediate – present on multiple continents but with historical strength in Australia and Europe (and a strategic exit from volatile Latin America). American Vanguard and Bioceres are more regionally concentrated (AVD’s core is U.S., Bioceres’ core is South America) and use partnerships or acquisitions to expand abroad. As a result, the big globals can leverage scale in distribution and manufacturing, whereas smaller players focus on niches where they can achieve critical mass (e.g. AVD in U.S. corn soil insecticides, Bioceres in Argentina’s biologics market).

Customer Segments and Go-to-Market: Most of these companies sell through similar ag retail/distributor channels, but their tactical approach differs. For example, Bayer and Corteva run loyalty programs and integrated offerings (often bundling seed and chemical deals for large farms), and they offer sophisticated agronomic support (through digital farming tools like FieldView or Granular). FMC and BASF emphasize technical service and product performance to compete for shelf space at retailers, sometimes partnering on custom solutions for large growers. Nufarm, dealing mostly in generics, often competes on cost-effectiveness and local relationships, working closely with distributors in each region to push volume. American Vanguard uses a mix of traditional distribution and its proprietary SIMPAS system (sold via equipment dealers) to create a unique channel for its products. Bioceres often leverages collaborations (e.g. co-marketing agreements with bigger firms in new regions) and a direct-to-grower model in its home market via field advisors demonstrating its biologicals.

M&A and Partnerships: Consolidation has been a big theme – Bayer’s mega-acquisition of Monsanto, ChemChina’s of Syngenta (not covered here due to being state-owned), and BASF’s asset buy from Bayer reshaped the industry around 2017–2018. Since then, Corteva and FMC have favored organic growth and bolt-on acquisitions (Corteva’s biologicals buys, FMC’s tech partnerships), while Nufarm divested major assets to focus, and Bioceres has been very acquisition-driven (merging with Marrone Bio, etc.). The result is that larger players have broadly diversified portfolios and are investing in emerging tech (digital, biological), whereas mid-sized ones are either narrowing their scope to core competencies (Nufarm to certain geographies/products) or trying to differentiate via technology (AVD’s precision ag tactic, Bioceres in biotech). Partnerships are also notable: almost every company has formed alliances in biologicals (e.g. FMC with Zymergen/Micropep, Corteva with Microbial Discovery ventures, BASF with Embrapa or other institutes) reflecting a recognition that collaboration can accelerate innovation in new fields.

Sustainability and Regulatory Adaptation: Strategies diverge in responding to regulatory and societal pressures. The European heavy companies (Bayer, BASF) are contending with the EU’s push to cut chemical pesticide use – BASF is shifting resources to friendlier markets and expanding its biological and digital portfolio in response. Bayer set public sustainability goals (like reducing environmental impact per hectare) guiding its R&D priorities. Corteva has likewise committed to sustainability targets (like training on safe use, developing greener chemistries) and made high-profile acquisitions in biologicals as a signal of this commitment. FMC and Nufarm also publicize sustainability – FMC is developing precision application models to reduce waste and investing in lower-toxicity products, and Nufarm’s Nuseed unit directly addresses sustainability via biofuel feedstocks (carinata) and omega-3 canola to ease pressure on fisheries. Meanwhile, smaller AVD emphasizes “GreenSolutions” as it modernizes its portfolio, and Bioceres is essentially built around sustainability (HB4 plants for climate resilience, microbial inputs to cut synthetic fertilizer needs).

📈 Historical and Forecast Growth Performance

Historical Revenue Growth (2019–2024): Over the last 5 years, industry growth was moderate, but individual company results varied due to events like acquisitions and divestitures:

Bioceres has been the standout, with exceptionally high historical revenue growth (5-year CAGR well into the double digits). This is largely because of its small base and transformative mergers – e.g. its revenue nearly tripled (~188% increase over 5 years) with the integration of Marrone Bio and organic expansion.

FMC Corporation’s growth latest data show revenue contracting by –13.42% year-over-year, with longer-term declines evident in a –13.60% three-year CAGR and –5.10% five-year CAGR. Even forward projections anticipate a further –4.17% drop in revenue, underscoring a clear downward trend. This performance positions FMC as a laggard in revenue growth among crop protection peers. FMC appears to have lost some market share amid these challenges. Larger rivals (Corteva, Bayer, BASF, etc.) with broader product portfolios and off-patent generic offerings have been able to better weather the downturn. Changes in FMC’s portfolio and product life cycle have also impacted growth. The company divested its small Specialty Solutions business in late 2024 to refocus on core crop chemicals. While strategically sound, this removed a minor revenue stream. More significantly, patent expirations are hitting key FMC products. Its blockbuster insecticide Rynaxypyr (chlorantraniliprole) is now off-patent in many countries, with full generic competition expected by 2026. This threatens an estimated $500 million in annual sales that Rynaxypyr contributed, as cheaper generic versions erode FMC’s volumes.

Corteva posted more modest revenue growth (low single-digit CAGR around ~4%). Since its formation in 2019, Corteva’s crop protection sales grew steadily but not dramatically – gains from new product launches were partly offset by currency headwinds and the loss of some older product lines. Additionally, Corteva’s overall growth is diluted by its large seed business (which had flat sales in some years). Nonetheless, crop protection within Corteva has grown faster than seeds, and recent years saw acceleration with new product uptake.

Bayer Crop Science saw below-average revenue growth. Excluding the one-time jump from acquiring Monsanto (2018), Bayer’s crop protection segment growth has been low or even flat. Roundup (glyphosate) experienced a boom in 2021–22 (price-driven) followed by a sharp decline in 2023, netting out to little growth over the period.

BASF Agricultural Solutions achieved moderate growth, partly front-loaded by the Bayer asset acquisition in 2018. Internal targets were ~5% CAGR through 2028, but actual performance has varied. In 2022 BASF’s ag sales grew ~26% (due to high prices and volume), but 2023 saw a decline with normalization. Over five years, BASF’s ag segment delivered low single digit CAGR. It wasn’t the fastest grower, but not the slowest either – essentially an industry-average performer historically.

Nufarm experienced a volatile and largely flat growth trend. Excluding divestitures, Nufarm’s continuing operations did grow in the low single digits, but currency swings and drought impacts meant minimal net growth.

American Vanguard also saw minimal revenue growth over the past five years. Its 2023 sales (~$579M) were only slightly above 2018 levels. Some years saw growth in certain segments, but overall AVD’s revenue has been essentially flat or oscillating with agricultural cycles. Supply issues (like the one-time spike and drop in Aztec insecticide sales) and portfolio rationalization kept its 5-year CAGR near 0%. Thus, AVD has been among the slowest growers (even contracting in 2023–24).

Expected Forward Growth (2025–2030): Looking ahead five years, industry analysts project modest growth overall, but with clear leaders and laggards:

Bioceres is expected to continue outpacing others in growth. As a high-upside company, consensus forecasts and company guidance suggest double-digit annual growth could persist for several years, driven by further geographic expansion of its biologicals and monetization of HB4 traits. While short-term sales dipped in 2025 due to macro conditions, Bioceres aims for a strong rebound and has set goals for ~40% gross margins and >20% EBITDA margins – implying aggressive top-line growth to achieve scale. Thus, Bioceres remains a leader in expected growth, potentially 15%+ CAGR going forward (in bull-case scenarios).

Nufarm is positioned for above-industry growth in the next few years, effectively from a low base. Having refocused and with new product opportunities (like its omega-3 canola and expanding European presence), Nufarm’s revenue is forecast to grow ~7–8% annually over the next 3 years. If it executes on its strategy to reach $600–700M EBITDA by 2026 (implying higher sales), its revenue CAGR could land in the mid to high single digits (~5–7%). This would make Nufarm one of the faster-growing mid-tier players, a turnaround from its stagnant past. However, this growth is partly a recovery from prior divestments and relies on margin expansion strategies.

FMC is expected to grow at a moderate pace. After a dip in 2024–25 due to channel inventory corrections, analysts anticipate FMC will resume growth as new products (like its novel herbicides) come to market and biological partnerships bear fruit. Consensus forward revenue CAGR may be in the mid-single digits (~4–6%), which is solid for a company of its size. This places FMC in the upper-mid pack – not as explosive as the smaller upstarts, but likely outpacing the largest conglomerates. Key drivers will be product mix improvement and emerging market demand.

Corteva’s forward growth looks to be in the mid-single digit range as well (perhaps ~4–5% annually for crop protection). The company has guided to mid-term sales growth above market rates, fueled by its pipeline of new chemistries (like novel insecticides and fungicides) and the ramp-up of biological sales from the Stoller/Symborg acquisitions. Corteva’s overall (including seeds) growth might be a bit lower, but in crop protection alone, it should see healthy increases. Thus, Corteva is around the industry average to slightly above in expected growth – steady if not spectacular.

Bayer Crop Science is generally expected to be a laggard in growth. Analysts forecast minimal revenue growth (on the order of 0–2% annually) for Bayer’s ag division through the mid-2020s. Glyphosate sales are not expected to rebound strongly, and while new product launches (traits, fungicides) add some revenue, they mostly offset expirations and price pressures elsewhere. Indeed, S&P projected Crop Science EBITDA margins flat through 2025 with revenue “less than 1%” growth in 2025. Unless Bayer makes a transformative move (like a spinoff that unlocks agility or a major new trait introduction), its crop protection segment is likely to trail the pack in growth.

BASF Agricultural Solutions should see low-to-moderate growth. The division has set a target of ~€12B sales by 2030 (from ~€9.8B in 2024) implying ~3–4% CAGR. External forecasts similarly suggest a modest mid-single-digit growth trajectory, given BASF’s strong pipeline and expansion in Asia, tempered by European market stagnation. So BASF is expected to grow roughly at the industry average (3–5% annually), not as slow as Bayer, but not high growth either.

American Vanguard presents a more unpredictable outlook. If its transformation succeeds, it could potentially grow revenues in the mid-single digits (perhaps ~5% annually), as it improves market share for key products and expands internationally (its CEO talks of returning to consistent growth). However, given its recent struggles, some forecasts might be more conservative or even flat. Thus, AVD’s forward growth is a question mark, but it’s generally not seen as a high-growth play – likely underperforming the broader market unless new products (or SIMPAS adoption) significantly boost sales. For now, it would be categorized among the laggards or at best average growth expectations.

🌐 Market Size Estimation: Bear, Base, and Bull Scenarios

Current Market Size: The global crop protection market (chemicals and biologicals combined, at ex-manufacturer value) in 2025 is estimated to be in the range of $60–70 billion annually. This reflects a slight cooldown from the 2021–2022 peak (~$69B in 2022) after exceptional price-driven growth, but overall the market remains on a growth trend over the long term. For scenario analysis, we use a 2025 base of ~$65 billion for ease of calculation.

Base Case: Steady, modest growth driven by population demand and incremental tech adoption. In a base-case scenario, the crop protection market might grow around 3–4% CAGR in the next 5–10 years. This assumes developing countries increase pesticide use moderately, new products (like biologicals and digital decision tools) add value, and pricing remains roughly in line with inflation. By 2030, a base-case market size could reach roughly $80–85 billion. For example, one industry report projects the market to grow from ~$64B in 2025 to ~$80B by 2033 (~2.9% CAGR) – our base case is slightly more optimistic, assuming 3.5% CAGR to hit about $82B by 2030.

Bear Case: Multiple headwinds constrain the market to low or near-zero growth. In a bear scenario – stringent regulations severely limiting chemical use (especially in Europe), major generic price erosion globally, plateauing farm incomes, and slow uptake of new technologies – the market might grow only ~1–2% CAGR, or even flatline in real terms. This could yield a 2030 market of around $70–75 billion. In dollar terms, that’s only incrementally above today. For instance, if growth is 1.5% annually, $65B in 2025 becomes about $70B by 2030. This scenario could occur if, say, large-scale bans on certain pesticides occur without equivalent higher-value replacements, or if a global recession squeezes agricultural investment.

Bull Case: A combination of strong demand and innovation drives accelerated growth. The bull scenario envisions ~6–8% CAGR over the coming years. Drivers would include high commodity prices spurring farmers to invest more in crop protection, rapid expansion of bio-based products creating new markets (rather than just substituting for older chemicals), and emerging markets (Africa, Asia) significantly increasing pesticide usage per hectare. Under a bull case, the market by 2030 could surpass $95–100 billion. For example, at 7% CAGR, $65B would grow to about $97B in five years. Some market research forecasts approach this: one source cites the broader “crop protection chemicals” market could reach ~$91B as early as 2023 and continue upward. Bullish assumptions might also factor in advanced digital farming greatly improving efficacy (so farmers confidently spend more on inputs knowing they’ll get returns) and climate change increasing pest pressures (requiring more treatments).

To summarize in scenario terms:

Bear Case: Limited growth. Market ~$72B by 2030 (approx. 1–2% CAGR).

Base Case: Moderate growth. Market ~$82B by 2030 (approx. 3–4% CAGR).

Bull Case: High growth. Market ~$100B by 2030 (approx. 6–7% CAGR).

Each scenario’s realized trajectory will depend on factors like regulation (a potential cap on chemical usage in key markets), technology (new products that either add value or face adoption hurdles), macroeconomics (farmer profitability), and sustainability pressures. Notably, biologicals are a wild card: They currently comprise only ~8–10% of the market but are growing ~3-4 times faster than conventional pesticides. If they achieve widespread adoption (bull case), they could expand the overall market value (since they often complement chemical programs rather than replace them entirely). Conversely, if regulations remove products faster than innovation can replace them (bear case), the market could stagnate or even shrink in certain regions (with volume down and only partial value replacement by pricier new tech).

It’s also useful to mention that while volume growth in pesticide use is low in mature markets, value growth can still occur via higher-priced innovations. The scenarios above incorporate both volume and price/mix effects. For instance, even in a flat volume environment, a shift to newer, more expensive products (like next-gen fungicides or bio-stimulants) could drive market value upward in the base or bull cases.

📊 Major Industry Trends and Growth Drivers

Several powerful trends and drivers are shaping the crop protection industry’s evolution:

Rise of Bio-Based Pesticides: There is a clear shift toward biological crop protection solutions – including biopesticides (microbial or botanical insecticides/fungicides), bioherbicides, and biostimulants. These products are gaining traction due to consumer demand for organic/low-residue food and regulators fast-tracking safer alternatives. Biopesticides, though still only ~8–10% of the market, are growing at an estimated >10% CAGR, outpacing conventional chemicals. All major companies have jumped on this trend: e.g. Corteva’s acquisitions of Stoller and Symborg, Bayer’s investments via its Biologicals division, FMC’s partnerships for microbial solutions. This trend is driven by improved efficacy of newer bio-products (some approaching parity with chemicals) and their integration into Integrated Pest Management (IPM) programs. We expect continued strong growth in bio-based inputs, expanding the market and also forcing traditional players to innovate or acquire in this space.

Stricter Regulations and Policy Shifts: Regulatory bodies, especially in Europe but also in regions like Brazil and parts of Asia, are raising the bar for pesticide approval. The EU’s hazard-based cutoff criteria and Farm-to-Fork strategy (targeting 50% pesticide use reduction by 2030) are emblematic of this. The result is a decline in the number of approved active substances in Europe and higher development costs for new chemicals. Elsewhere, regulations on residues and environmental impact are tightening. For example, certain neonicotinoids and organophosphates have been banned or restricted in multiple countries. These regulatory shifts push the industry towards safer, lower-dose chemistries and biologicals, and also contribute to consolidation (only large firms can afford the costly, lengthy registration processes). In some cases, regulations create market volatility – e.g. glyphosate legal battles in the US causing uncertainty, or India and China periodically banning or restricting exports of key ingredients. In summary, a more stringent regulatory climate is both a driver of innovation (to meet new standards) and a potential growth limiter (if products are removed faster than new ones come).

Digital Agriculture and Precision Application: The proliferation of digital farming technologies is influencing crop protection usage. Platforms like Bayer’s Climate FieldView, BASF’s xarvio, and independent agtech tools provide farmers with real-time data and predictive analytics on pest pressures, weather, and optimal spray timings. This enables more precise and targeted pesticide use – for instance, variable rate application by zone, or predictive models that spray only when disease risk is high. Drones and smart sprayers with sensors (some leveraging AI for weed recognition) are also emerging, allowing micro-targeting of pests. Digital tools can potentially reduce over-application (a sustainability win) while ensuring effective control, thereby preserving product demand by proving ROI. Companies are leveraging digital as a differentiator: e.g. Syngenta and FMC’s investments in farm management software, Corteva’s Granular platform, etc. Over time, digital ag should drive growth by optimizing input use (convincing skeptical growers to adopt novel products through demonstrated outcomes) and by enabling new service-based revenue models (e.g. “outcome-based” pricing for crop protection tied to digital monitoring). It also favors companies that integrate these solutions with their product sales.

Herbicide Resistance and Resistance Management: A major agronomic driver is the spread of pest resistance to existing pesticides. Weed resistance to glyphosate and other herbicides has become a serious problem globally, and insects/diseases likewise develop resistance to chemistry over time. This creates an urgent need for new modes of action and combination strategies, effectively driving demand for newer products. FMC’s introduction of a new MOA herbicide, or Bayer developing a next-gen herbicide, are direct responses to glyphosate-resistant weeds. Likewise, resistance management is spurring stacked products (premixes of multiple actives) and rotational programs – which often means using a higher variety of products across seasons. As resistance issues mount (which they will, given intensive usage patterns), growers must invest in more robust control measures, supporting industry growth. However, resistance also erodes efficacy of old staples, pushing them out in favor of new solutions. Companies that can bring novel modes (chemical or biotech, like RNAi traits for insect control) stand to gain. This dynamic is a key driver for innovation and a constant undercurrent in farmer purchasing decisions.

Climate Change and Emerging Pest Threats: Climate change is altering pest patterns and pressure. Warmer temperatures and changing rainfall can expand the range of certain pests (e.g. invasive insects moving into higher latitudes) and intensify crop disease cycles. We’re seeing new challenges like fall armyworm spreading to Asia/Africa, or unexpected locust surges. These threats drive demand for crop protection in regions that previously had lower usage or for crops that now face new pests. Conversely, climate stress also increases interest in resilient solutions (drought-tolerant traits, stress mitigants), indirectly benefiting companies like Bioceres. Additionally, extreme weather can cause pest outbreaks following floods/droughts, requiring emergency pesticide applications. Thus, climate volatility often increases the reliance on crop protection to secure yields. On the flip side, climate concerns also push the industry toward more sustainable practices (to mitigate agriculture’s footprint), reinforcing trends toward integrated pest management and low-impact products.

Consolidation and Changing Industry Structure: The last decade saw massive consolidation – the “Big 6” became the “Big 4” (ChemChina/Syngenta, Bayer/Monsanto, Corteva, BASF, plus FMC and others). This consolidation has generally increased the scale of R&D and global reach among the top players. It also led to portfolio shuffling (divestments to satisfy antitrust, which allowed companies like BASF and FMC to expand). Now, a few firms control a large share of patented products, and generic manufacturers (many in China, India) control the bulk of off-patent volume. Looking ahead, we see continued consolidation at various levels: distributors merging (vertical integration in the value chain), and possibly more acquisitions of biopesticide startups by big agchem companies. However, we also see new entrants (startups) bringing disruptive tech (e.g. RNAi sprays, microbiome solutions) – often these entrants get absorbed by larger companies once proven. Overall, the industry is bifurcated between big integrated companies and a competitive fringe of generic makers, which drives differing strategies. Consolidation has made the big players more financially robust to invest in next-gen products, a positive for innovation, but it has also raised concerns about market power and farmer choice.

Focus on Sustainability and ESG: Both as a response to external pressure and internal corporate responsibility, all major players are embedding sustainability into their strategies. This includes targets to reduce greenhouse gas emissions in manufacturing, to develop climate-friendly products, and to help farmers sequester carbon (e.g. Bayer’s carbon farming initiative where farmers get paid for practices and possibly use specific inputs). It also involves stewardship programs to train farmers in safe and judicious pesticide use (often led by companies to pre-empt regulatory criticism). Sustainability trends drive investment into alternative pest control methods like pheromone disruptors, trap crops, and biologically derived chemistries. They also mean companies are reconsidering product portfolios – for instance, several firms voluntarily discontinued highly toxic products (like Corteva ending chlorpyrifos production). ESG metrics are increasingly used by investors to evaluate these companies, serving as a growth driver for those who adapt (they may attract “green” investment or avoid certain bans) and as a risk for laggards.

Emergence of Integrated Pest Management (IPM): Farmers and regulators are increasingly promoting IPM approaches – combining chemical, biological, and cultural techniques to manage pests. This trend doesn’t eliminate the use of pesticides but changes the product mix and timing. For example, a farmer might use a seed treatment and beneficial insects to keep pest levels low, resorting to chemical sprays only when thresholds are exceeded. Leading companies are repositioning as “solution providers” to fit into IPM regimes – selling not just a bottle of chemical, but a package (perhaps including a monitoring tool, a bio-stimulant to strengthen crop, and a targeted spray). Those adapting well can still thrive in an IPM-heavy world by ensuring their products complement rather than compete with non-chemical methods. IPM’s rise is also supported by technology (drones scouting fields, AI identifying pests early). In sum, IPM is changing how products are used – pushing the industry to provide more knowledge-driven support and diversified product portfolios.

These trends collectively point toward a future crop protection industry that is more technologically advanced, environmentally conscious, and dynamic. Traditional chemical pesticides remain crucial, but their development and use are increasingly influenced by these broader drivers.

🎯 Key Success Factors and Profitability Drivers

Profitability in the crop protection sector varies widely by company, but several core factors drive higher margins and returns:

Product Portfolio Mix (Patented vs. Generic): Perhaps the single biggest driver of profitability is the share of proprietary, patent-protected products a company sells. New, patented active ingredients enjoy pricing power and high gross margins, whereas off-patent (generic) products face price competition and commoditization. For example, a patented novel fungicide or a unique herbicide trait system can command premium prices and high EBITDA contribution. In contrast, common generics like glyphosate have slim margins due to numerous suppliers. Industry-wide, patented products now make up only ~10% of the market value, meaning most sales are from off-patent actives – this shift to ~70%+ generics has pressured margins across the industry. Thus, companies like Corteva, BASF, FMC that continually launch new AIs or formulations tend to sustain higher profitability, whereas those reliant on legacy generics (Nufarm, many Chinese firms) operate at lower margin. The ability to differentiate products (via formulation technology, premixes, or brand trust) also helps sustain pricing on off-patent products, aiding profitability.

Scale and Operational Efficiency: The large fixed costs in this industry – R&D labs, regulatory trials, manufacturing plants – mean that scale economies significantly impact profitability. Global players manufacturing at high volumes can achieve lower per-unit production costs, and they can spread R&D expenses over a bigger revenue base. This often yields higher EBITDA margins for bigger companies (with exceptions for conglomerates burdened by overhead). Operational excellence in supply chain and procurement (like securing raw materials at low cost) also boosts gross margins. Many crop chemicals are petroleum or commodity-chemical derivatives, so sourcing efficiency and process engineering matter. Companies with vertically integrated production for key intermediates (e.g. BASF, Bayer produce some raw materials internally) can have an edge. Conversely, smaller firms that must buy intermediates at market prices or operate subscale factories struggle with higher unit costs. This is why American Vanguard, for example, has been targeting a transformation to improve efficiency and lift its margin from ~7% toward 15% – chasing what scale peers achieve.

Geographic and Crop Mix: Profitability can be influenced by where and what a company sells. Developed markets like North America and Europe often allow for higher pricing (due to higher regulatory compliance costs and customer willingness to pay for advanced products), supporting better margins. Emerging markets drive volume but sometimes at lower pricing or higher credit risk. A balanced geographic mix helps – for instance, Syngenta (not public) and Bayer have benefitted from strong margins in Latin America during currency swings by pricing to offset FX. Crop-wise, servicing high-value fruit/vegetable segments can yield higher margins than bulk commodity crops, as specialty growers pay premium for tailored solutions. So a company with a good share of specialty business (e.g. part of FMC’s portfolio, or AVD’s non-crop segment) might see improved margins. However, too much reliance on any one region or crop can hurt profitability if problems arise (like AVD’s over-reliance on U.S. corn soil insecticides – when that market dipped, overheads dragged down profit).

Portfolio Life Cycle Management: How well a company manages the life cycle of its products impacts profitability. Leading firms time the introduction of new AIs such that as older ones go off-patent and experience margin erosion, newer high-margin products ramp up to replace them. They also use strategies like reformulation or combining products into premixes to extend the profitable life of off-patent products. (Premixes of multiple actives can be patented as a combination, or at least allow value-based pricing for the convenience/effectiveness, thus maintaining higher margin than selling each generic alone.) For example, proprietary premixes in crop protection are common and often carry a margin uplift. Companies that are agile in this (FMC, Corteva, BASF) sustain margins better than those that let products commoditize without replacement. Also, managing the tail of the portfolio – discontinuing low-margin, high-regulation-cost products – can remove profit drags and free resources. Nufarm’s sale of low-margin regional assets is one such move to improve overall margin profile.

Innovation and R&D Productivity: The R&D efficiency – turning research dollars into successful, commercially valuable products – drives long-term profitability. A breakthrough product can generate hundreds of millions in profit during its patent life. Companies with strong discovery pipelines (like Bayer, Corteva, FMC) aim for a steady cadence of such launches. However, R&D is expensive (major firms spend ~8–10% of sales on R&D), so the success rate matters. If a company’s pipeline fails to produce enough winners, that R&D spend becomes a drag on margins. On the other hand, firms that excel in picking and developing winning candidates see a huge payoff (the ROI on a new blockbuster AI is very high). Additionally, innovation in adjacent areas like formulation science (making products more effective or easier to use) can justify premium pricing and higher margin. For instance, controlled-release formulations or safe-handling packaging may allow a company to charge more for essentially the same active ingredient, boosting profitability.

Manufacturing & Supply Chain Integration: Crop protection chemicals manufacturing can be complex (multi-step chemical synthesis) and capital-intensive. Profitability is higher for companies that optimize their manufacturing footprint – either by locating plants in low-cost regions, ensuring high capacity utilization, or outsourcing strategically. Some companies like Syngenta and Bayer operate large-scale plants in Asia or Eastern Europe for cost advantage. There’s also the aspect of supply reliability: in recent years, supply disruptions from China (a key source of generic AI production) have driven prices up. Companies that could ensure supply (either via own production or strong supplier contracts) could capitalize on higher prices without stock-outs. For example, in 2018–2019, when China’s environmental crackdown cut generic output, firms with captive production benefited. Conversely, those caught buying on the spot market faced squeezed margins. Thus, an efficient, secure supply chain adds to profitability by both lowering cost of goods and enabling sales in tight markets.

Generic Competition and Pricing Discipline: An industry-level profitability factor is how companies respond to generic competition. When a patent expires, if the original company slashes price to maintain volume, margins erode quickly. However, some companies choose to differentiate and maintain higher prices for their branded version while letting generics take the low end – essentially segmenting the market. The ability to do this depends on brand loyalty and formulation differences. Pricing discipline in the face of generics can preserve margin at the cost of some volume. Additionally, companies often reduce manufacturing costs of older products before patent expiry to remain competitive. Those that manage this transition smoothly (like continuing to produce at scale for a while and serving markets where brand trust is high) can still garner reasonable margins on “mature” products.

Product Stewardship and Liability Management: Avoiding major legal liabilities or product recalls is also key to maintaining profitability. Bayer’s glyphosate litigation is a prime example – it has incurred billions in provisions and legal costs, directly hitting profitability of that business. Companies invest in stewardship (training, label compliance, monitoring adverse effects) to minimize such risks. Generally, products with favorable safety profiles not only face less regulatory cost but also reduce the risk of expensive lawsuits or abrupt market withdrawals, thereby providing more stable profits.

💼 Porter’s Five Forces Analysis

Applying Porter’s Five Forces to the global crop protection industry illustrates the competitive dynamics and challenges:

Threat of New Entrants: LOW. The crop protection market has high barriers to entry. Developing a new chemical active ingredient is R&D intensive (often $250M+ and a decade of testing) and requires navigating stringent global regulatory approvals – a formidable hurdle for newcomers. Existing players have established distribution networks and brand trust with farmers, which new entrants would struggle to replicate. Additionally, intellectual property (patents) protects novel products for years. While a small startup might enter with a specific innovation (especially in niche areas like biologicals or digital tech), it usually must partner with or be acquired by incumbents to scale. Generic manufacturing of off-patent chemicals is easier to enter (some Indian and Chinese firms do so), but even there, economies of scale and compliance costs limit viable entrants. Overall, new entrants face high capital needs, regulatory barriers, and the need to overcome customer loyalty to incumbent products – therefore the threat remains low. The exception is in emerging segments like biopesticides, where regulatory barriers are slightly lower; even so, major agchem companies are acquiring or outcompeting most upstart biopesticide firms.

Threat of Substitutes: MODERATE. Farmers ultimately want healthy crops, and crop protection chemicals are one means to that end. Substitute solutions include non-chemical pest control methods (crop rotation, biological control via natural predators, mechanical weeding, resistant crop varieties, etc.) and even consumer-driven changes like organic agriculture (which avoids synthetic pesticides). In many cases, these substitutes are used in tandem (IPM) rather than outright replacing chemicals, but they can reduce reliance. For example, genetically modified Bt crops substantially reduced the need for external insecticide sprays for certain pests – a substitute effect provided by seed technology. Likewise, precision agriculture enabling micro-targeting of pests can substitute blanket chemical applications with more efficient, lower volumes. The success of organic farming (still a small fraction of total acreage globally) is a niche threat but shows some willingness to try farming with minimal chemicals, often substituting labor or biological methods. However, for large-scale commercial agriculture, completely eliminating chemical crop protection is very challenging; substitutes often are complementary or not as cost-effective at scale. Thus, while the array of substitutes (cultural, mechanical, biological controls) creates a moderate pressure – pushing companies to innovate and reduce chemical usage per acre – these alternatives are unlikely to wholly displace the need for crop protection products, especially as global food demand rises.

Bargaining Power of Suppliers: LOW to MODERATE. Key suppliers to crop protection firms include chemical raw material providers (basic chemicals, intermediates), specialized fine chemical manufacturers, and to some extent, producers of formulation ingredients or packaging. Many raw materials are commodity chemicals (solvents, acids, etc.) available from multiple sources globally, which limits supplier power. Some intermediate chemicals (precursors specific to an active ingredient synthesis) might have only a few qualified suppliers, giving those suppliers moderate leverage – but large agchem companies often hedge this by dual sourcing or manufacturing critical intermediates in-house. The rise of China and India as major low-cost suppliers of generic actives and intermediates has actually shifted power towards crop protection companies, who can shop around for best prices. In cases where production of a certain technical grade active is concentrated (e.g. if one big Chinese factory supplies a large share of a generic), a disruption can spike prices, but generally the buyers (agchem companies) have negotiation power due to volume and alternative options. Additionally, big players like BASF, Bayer, Corteva often have backward integration or long-term contracts mitigating supplier influence. On the flip side, if environmental regulations shut down multiple suppliers (as happened in China for some fine chemicals), suppliers can temporarily gain leverage. Overall, supplier power is relatively low; they tend to compete on price for the business of large crop protection firms.

Bargaining Power of Buyers: MODERATE. The end-users of crop protection products are farmers, who are numerous and fragmented in most regions (millions of farms worldwide). Individual farmers typically don’t have much leverage over giant suppliers. However, farmers are price-sensitive and can switch between brands or generic equivalents if available, which tempers pricing power of companies. The distribution channel adds another layer: large ag input distributors and retailers (e.g. Nutrien, Helena in the US; co-ops in Europe; national distributors elsewhere) aggregate demand and can negotiate for volume discounts or promotional deals. These distributors have moderate bargaining power, especially as they consolidate – a few big distributors can influence which products get shelf space. Additionally, in some markets, government buying agencies or subsidies influence purchases (e.g. government tenders for locust control pesticides, or government price controls in India on certain pesticides), which can reduce pricing flexibility. Farmers can also choose alternative strategies – if chemical prices rise too much, they might plant different crops or use more of a substitute method (giving them indirect leverage). Nevertheless, the differentiated value of patented products and the relatively small cost of pesticides compared to crop revenue limit buyer pushback (if a fungicide prevents a 20% yield loss, a farmer will pay for it). Weighing these factors: buyers have some power through choice and channel intermediaries, but not to the extent of commoditized industries. It’s a moderate force – stronger for generic products (where buyers can easily switch to a cheaper source) and weaker for unique solutions.

Competitive Rivalry: HIGH. The crop protection industry is highly competitive, marked by both oligopolistic competition among big R&D firms and intense price competition in generic segments. A handful of large companies (Bayer, Syngenta, Corteva, BASF, FMC, UPL) dominate the patented product space, and while they compete on innovation and global market share, they tend to avoid destructive price wars on new products. However, once products lose exclusivity, they enter a fiercely competitive generic arena with numerous producers (especially from China/India) driving prices and margins down. The market is also relatively mature (global growth in volume is slow), so gaining sales often means stealing share from a competitor rather than expanding the pie, fueling rivalry. In recent years, rivalry has also played out in legal and regulatory spheres – companies filing lawsuits or petitions (e.g. Corteva’s petition on 2,4-D anti-dumping shows competitive tactics to constrain cheap imports). There’s competition in innovation too: being first to market with a new mode of action or trait can capture outsized value, so companies race in parallel, sometimes forming alliances (like FMC and Syngenta co-developing a herbicide for rice, balancing cooperation and rivalry). The presence of many generic firms ensures price-based rivalry is intense for off-patent products – margins slim down as soon as multiple players sell the same AI. Meanwhile, the big companies compete via product performance, service, and bundling (traits + chemicals) to lock in customers. High fixed costs and R&D sunk costs also encourage companies to aggressively push volume (to amortize costs), sometimes leading to oversupply in certain markets and consequent price competition. Overall, rivalry is high and multi-dimensional – from pricing battles in commoditized products to innovation battles for the next big solution – making this a strong force in the industry.

In summary, the Five Forces analysis indicates an industry with formidable entry barriers and moderate supplier leverage, but significant internal competition and some pressure from buyers and substitutes. The combination of high rivalry and widespread generic availability keeps profit potential in check, meaning companies rely on innovation (to escape pure price fights) and scale to thrive. Those with differentiated offerings can mitigate some of these forces (e.g. reducing buyer power and rivalry for their unique product), whereas those stuck in commodity segments face the full brunt of competitive and buyer pressures.

💵 Financial Metrics Analysis (Profitability & Efficiency)

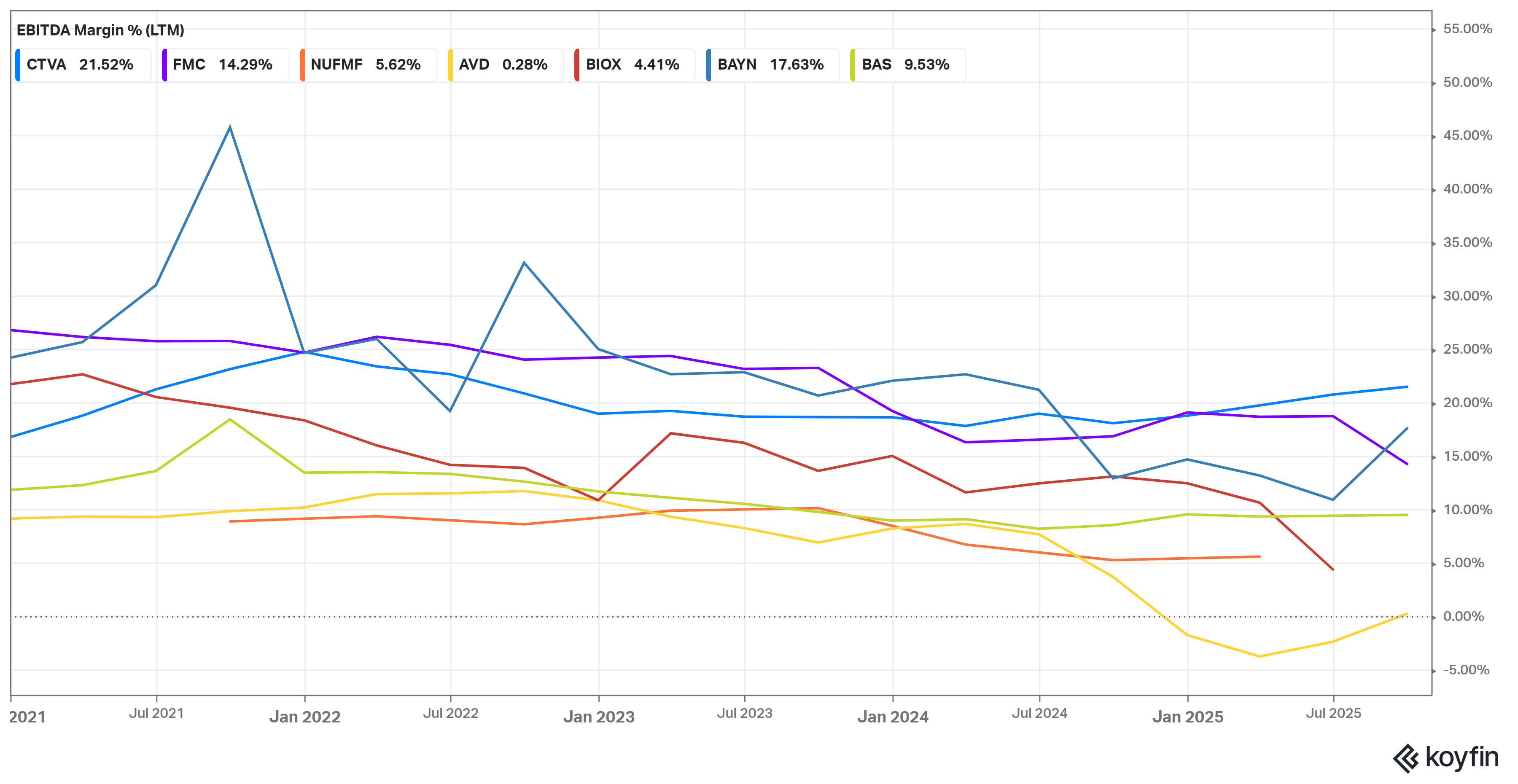

EBITDA Margin (LTM): EBITDA margin reflects core profitability before depreciation and amortization. Among these peers, FMC Corp. stands out with one of the highest EBITDA margins, roughly in the low-to-mid 20s (%) LTM, making it a top performer. FMC’s focus on high-value patented products and cost discipline has historically yielded EBITDA margins above 22%, slightly edging peers. Corteva has significantly improved its EBITDA margin – achieving ~20% in 2024 – thanks to pricing actions and cost synergies, putting it in the upper tier as well. Bayer’s crop science EBITDA margin was around ~19% in 2024, and BASF’s ag segment ~20%, both in a similar ballpark just under FMC. The lowest EBITDA margins are seen in Nufarm and American Vanguard. Nufarm’s EBITDA margin has been in single digits in recent years (around 8–10% underlying in FY2024), reflecting its still-heavy generic portfolio and improvement journey. American Vanguard’s EBITDA margin turned negative in the LTM due to one-time charges and weak sales – it reported a small negative EBITDA margin (~-2% TTM)s, making it a bottom performer. Even on an adjusted basis excluding one-offs, AVD’s margin (~7–8%) is the lowest of the group. Bioceres’ LTM EBITDA margin is moderate, roughly in the low-to-mid teens (around 10–15%), reflecting its growth-company investment mode – better than Nufarm/AVD but below the large peers.

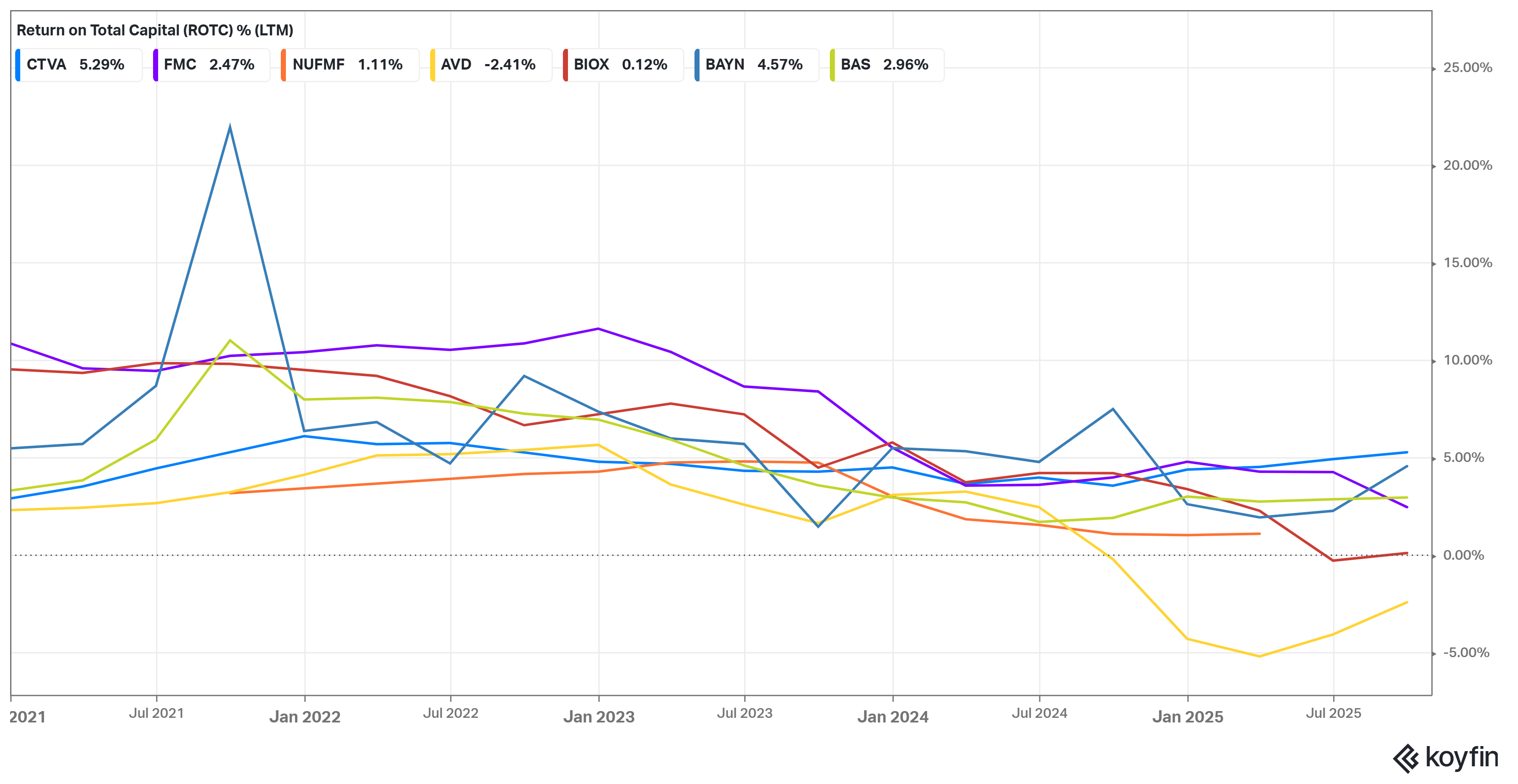

Return on Total Capital (LTM). FMC emerges as a leader on this metric. With its relatively high margins and not overly bloated asset base (after divesting lithium, it’s focused and not carrying excess intangible weight like some peers), FMC’s return on capital is strong – likely in the low double digits percentage-wise. In 2022–2023, FMC’s ROIC was often cited around 10–12%, which would outpace many competitors. Corteva’s ROTC has been improving – initially low after the spin (due to large intangibles from the merger), but as earnings have grown, its ROIC has risen. Still, Corteva’s return on assets was ~3.5% (ttm ROA) and ROIC might be mid-single-digit historically; by 2024 it’s probably approaching high single digits. The very large companies Bayer and BASF have relatively weak ROTC for different reasons: Bayer’s crop science division carries a huge goodwill/intangible from Monsanto, which means capital employed is massive relative to earnings – S&P projected Crop Science ROCE staying around mid-single-digits given ~19% EBITDA margins and asset intensity. BASF’s ag segment is reasonably profitable, but as part of BASF it’s weighted down by significant capital (including the 2018 acquisition cost); its ROTC might be moderate (perhaps 5–7%). Bioceres and American Vanguard currently deliver poor or negative returns on capital. Bioceres is not yet consistently profitable, so its return on capital is low (it has significant goodwill from acquisitions like MBI, and still minimal profits – a subpar ROIC around low single or negative). AVD’s recent losses mean negative net returns; even on an adjusted basis its ROIC would be very low. Nufarm’s ROTC is also likely low-single-digit; after asset sales it reduced capital, but earnings have been thin.

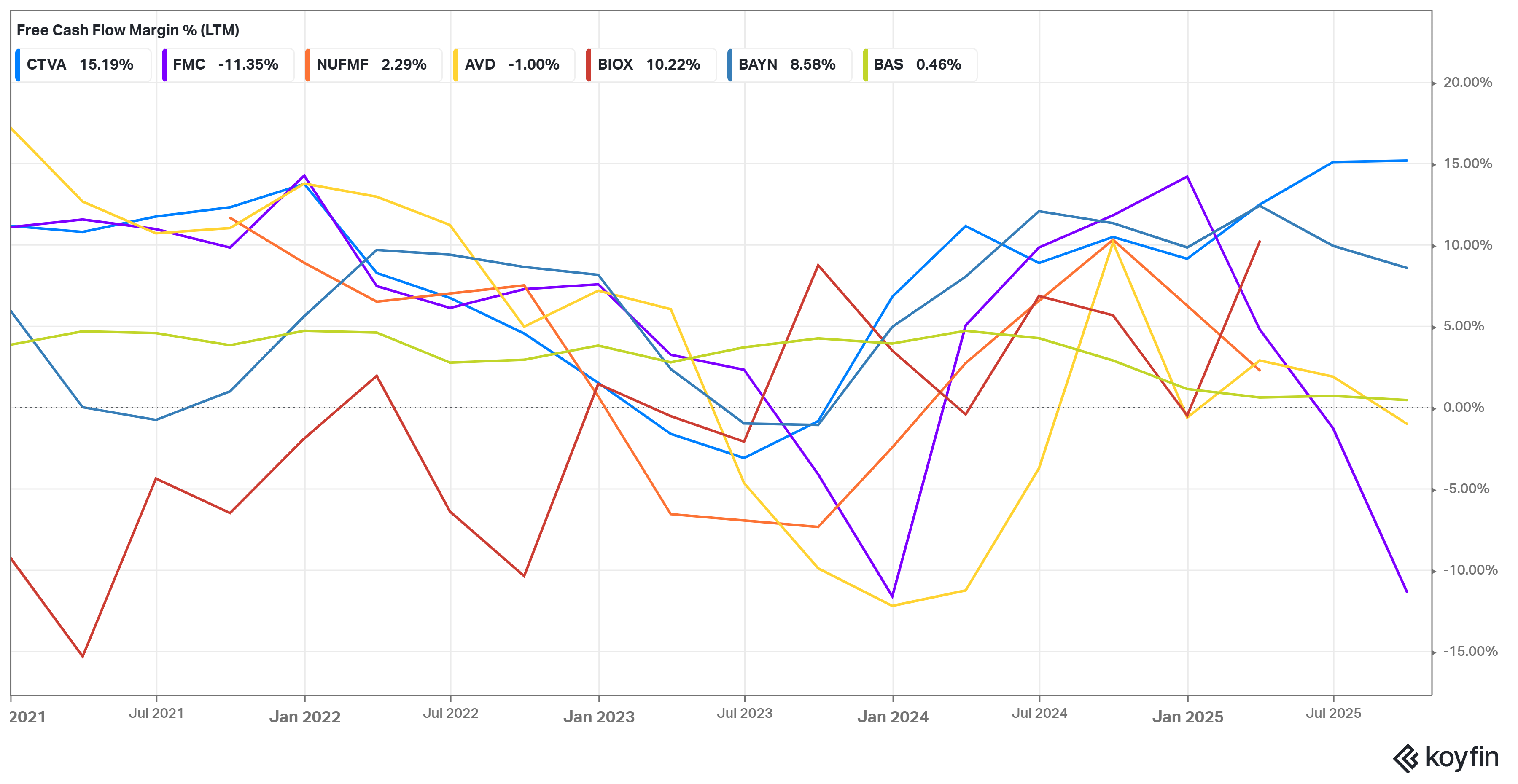

Free Cash Flow (FCF) Margin (LTM). Corteva and FMC appear as leaders in FCF generation. Corteva’s strong operating cash flows (aided by its seeds business’ seasonality and disciplined capex) have given it a healthy FCF margin in recent periods – it consistently converts a large portion of EBITDA to free cash, reflecting efficient working capital use post-spin. FMC, likewise, historically prided itself on high cash conversion, though it faced some challenges with inventory build in 2023. Nonetheless, FMC’s FCF margin is relatively robust given its asset-light approach (manufacturing outsourcing) and moderate capex requirements; we can infer it has been in double digits (%) in better years. Top performer in FCF margin might actually be Corteva recently, as it benefited from one-time working capital tailwinds – reports suggest Corteva’s cash flow generation has been strong in 2024, with free cash flow exceeding net income. On the other hand, Bioceres and American Vanguard are bottom performers on FCF. Bioceres, due to growth investments and working capital for expansion, had negative free cash flow in the LTM (it reported net losses and is investing in inventory and integration), so its FCF margin is poor. American Vanguard also has struggled to generate free cash – stock analysis indicated an FCF margin under 2% TTM for AVD, meaning it barely produces free cash. Nufarm’s FCF margin is also traditionally low or volatile; high working capital (typical for generic businesses with seasonal sales) eats into cash flow, and Nufarm often has had to manage debt. In FY2024, Nufarm did reduce net debt, implying some positive free cash, but margin-wise it’s likely modest. Bayer’s crop science and BASF ag, being parts of bigger firms, are harder to parse, but generally, heavy capex and substantial working capital in these giants can depress FCF conversion relative to EBITDA. For instance, Bayer AG’s overall FCF has been impacted by litigation payouts and integration costs.

In each metric, we see a common pattern: the companies that focus on high-value, differentiated products (and have achieved scale efficiencies) – FMC, Corteva – tend to score well, whereas those dealing with portfolio or scale challenges – Nufarm, AVD – lag behind. Bioceres, being in growth mode, currently looks weak on pure financials, but that’s expected for an emerging company investing for future returns. Bayer and BASF, despite their size, show only middling performance on returns due to integration of huge acquisitions and mixed portfolios (plus one-time issues like litigation for Bayer).

🥇 Conslusion - Leaders, High-Upside, and Weak/Volatile Players

Based on the full analysis of strategic positioning, growth, and financial performance, we can categorize these companies into three groups:

Capital-Efficient and Cash-Generative Leaders: These are companies that demonstrate strong profitability, disciplined capital use, and reliable cash flows – effectively the blue-chip operators in crop protection. FMC Corporation clearly falls in this category: it has consistently high EBITDA margins, robust free cash flow conversion, and solid ROIC, reflecting a well-managed pure-play with a focus on innovation and cost control. Corteva, Inc. can also be included here as of recent performance – after a transformative spin-out period, Corteva has reached the 20% EBITDA margin milestone, generates substantial cash (helped by its seeds business synergy), and leads in integrated solutions. Corteva’s balanced approach and improving returns make it a cash-generative leader (with the caveat that it’s reinvesting heavily in R&D too). BASF’s Agricultural Solutions segment, while part of a larger entity, is relatively capital-efficient and profitable as well – it consistently delivers ~18–22% EBITDA margins and good cash generation within BASF. If standalone, it would likely be viewed as a leader given its stable margins and innovation pipeline, though currently its value is masked within BASF. These leaders are characterized by strong competitive moats (proprietary products, global reach) and the ability to fund growth internally while returning cash to shareholders (e.g. dividends, buybacks in FMC and Corteva’s cases). They tend to be lower risk and set the industry’s performance benchmark.

Growth-Focused Companies with High Upside Potential: This group comprises players prioritizing expansion, innovation, and market share growth, even at the expense of near-term margins. They have significant upside if successful, but also higher risk. Bioceres Crop Solutions epitomizes this category – it’s aggressively growing its sustainable ag portfolio and could see outsized gains as HB4 wheat and its biological solutions scale globally. Investors in Bioceres are betting on high revenue CAGR and eventual margin expansion from ~15% to 20%+, which could dramatically improve earnings. Nufarm Limited can also fit here: after restructuring, Nufarm is in growth mode with ambitions to nearly double EBITDA by FY2026. It is focusing on developing unique niches (like omega-3 canola, carinata biofuel feedstock, and bolstering its core crop protection range) and expanding in North America/Europe. If Nufarm achieves its margin and growth targets, there’s significant upside from its currently subdued profit levels. However, it remains somewhat volatile (weather and currency-exposed), so it straddles this high-upside category. One might also consider Bayer Crop Science as a variant in this group: while currently underperforming, Bayer has a vast innovation pipeline (including cutting-edge traits and digital initiatives) and if it resolves litigation and executes on new product launches, its growth and margin could improve significantly from current lows. The upside scenario for Bayer’s ag division (perhaps under new leadership or in a spin-off) could be substantial given its R&D scale. Thus, Bayer could be seen as a turnaround/growth opportunity – though not “growth-focused” by choice, it has the elements to rebound, making it appealing if one looks past current issues. These high-upside companies offer potential for above-market growth and valuation increase if their strategies play out, but they require careful execution and often involve higher leverage or investment needs (hence present more variability in outcomes).

Structurally Weak or Volatile Players to Avoid: Companies in this bucket are characterized by either inherent structural disadvantages (small scale, heavy reliance on commoditized products, financial instability) or highly inconsistent performance, making them higher risk with comparatively lower reward. American Vanguard Corporation unfortunately falls here. With its sub-scale revenue base, aging product lineup (many off-patent chemistries facing generic pressure), and recent string of low or negative earnings, AVD appears structurally weak. It is in the midst of a transformation, but until there’s tangible proof of sustained margin improvement and growth, investors may prefer to avoid or be cautious. The company’s volatility (a big swing from slight profit to large loss due to one bad season and one product recall) highlights its fragile position. Another candidate for this category is the generic-heavy segment of the market in general – Nufarm might have been here prior to its refocus, but it’s attempting to leave this category through its strategic changes. Within our scope, if one were to isolate Bayer’s situation, some might argue Bayer is a “volatility to avoid” in the near term given the ongoing glyphosate litigation, margin pressures, and the fact that its conglomerate structure is depressing returns (net losses at group level recently). However, Bayer’s crop science is not structurally weak in terms of assets – it’s more a strong business under a cloud. Nufarm still has some structural challenges (no patented blockbusters, lower scale than top rivals, exposure to climate swings in Australia), so if its transformation falters, it could remain in a weaker position – but the expectation of improvement puts it more in the upside group for now. So, the clearest avoid/weak player is American Vanguard, which currently lacks the scale, differentiation, or financial strength of others. Investors would likely steer clear until it proves it can consistently generate profits and cash (i.e. complete its “halfway to full potential” turnaround, as management calls it).